Europe Is Investing Billions in Quantum, But Does It Have the Leadership to Scale? By The Big Search & UVC Partners

We collaborated with UVC Partners and mapped the backbone of the European quantum industry.

For Google CEO Sundar Pichai, quantum is the most exciting thing on the horizon. He could have said AI, autonomous driving. Instead, he mentioned quantum.

In Europe, quantum startups are raising more capital each year, dedicated VC funds are launching, and companies are gaining traction. IQM, Pasqal, and Quantinuum have announced plans to IPO. The way we see it, it’s an opportunity to unlock new capital and acquire smaller software or cooling-tech startups to build more vertically integrated companies.

But is the talent keeping pace?

Previously on The Big Byte, we looked at the European quantum ecosystem through the lens of IQM’s and Quantinuum’s talent structure. This time, we mapped the backbone of the industry across 237 European quantum companies, spanning:

Quantum computing software, algorithms & simulation

Quantum computing hardware

Quantum sensing & metrology

Quantum communications, networking & cryptography

Quantum enabling technologies (photonics, cryogenics & control)

We identified 900+ individuals across founders, current C-levels, and current commercial leaders. We included commercial talent because generating revenue will be a major challenge for quantum startups, especially those going public. We looked at the composition of each talent pool, their experience in the sector, and where the European quantum industry sources its talent.

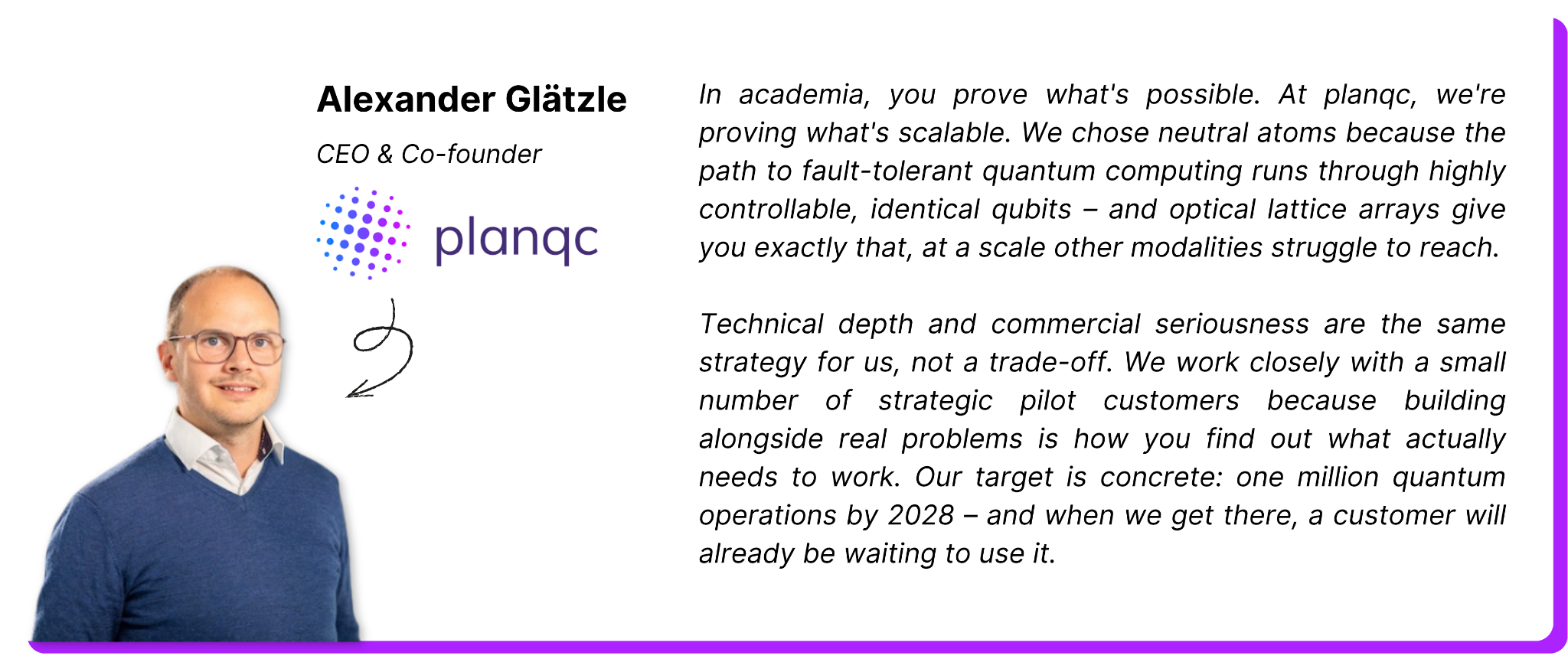

We partnered with UVC Partners on this piece. Amanda Birkenholz, Principal, and Benjamin Erhart, Partner, brought their investment perspective. Alexander Glätzle, CEO and co-founder of planqc, a UVC Partners portfolio company, also contributed.

Important note: We spoke with physicists while working on this piece, but we won’t pretend to be quantum experts. First and foremost, we are headhunters. Physicists know far more about quantum than we do, and that’s exactly why we work with companies to hire them. Enjoy the reading!

This article was compiled in collaboration with the DeepTech Practice at The Big Search. If you’re interested in leadership and talent trends, looking to hire a DeepTech leader, or simply want to discuss the findings, feel free to reach out: elena@thebigsearch.com or Elena Obukhova.

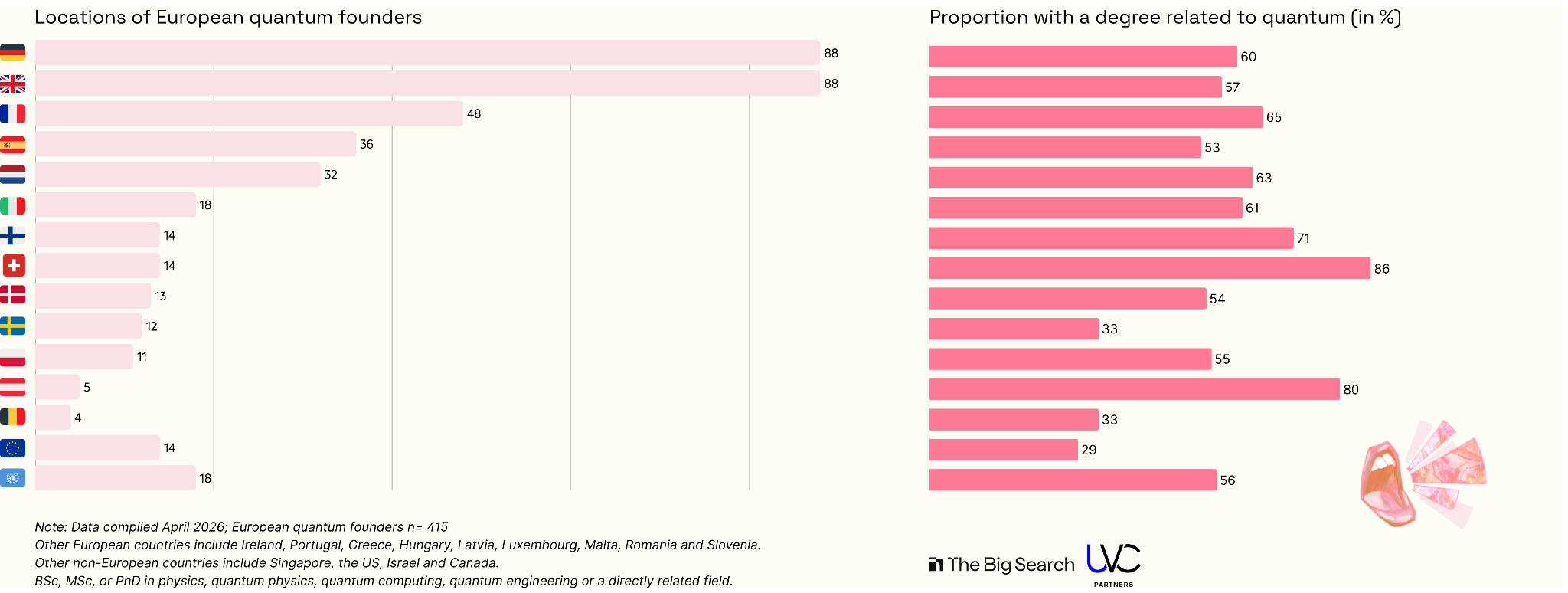

Most quantum founders hold a PhD

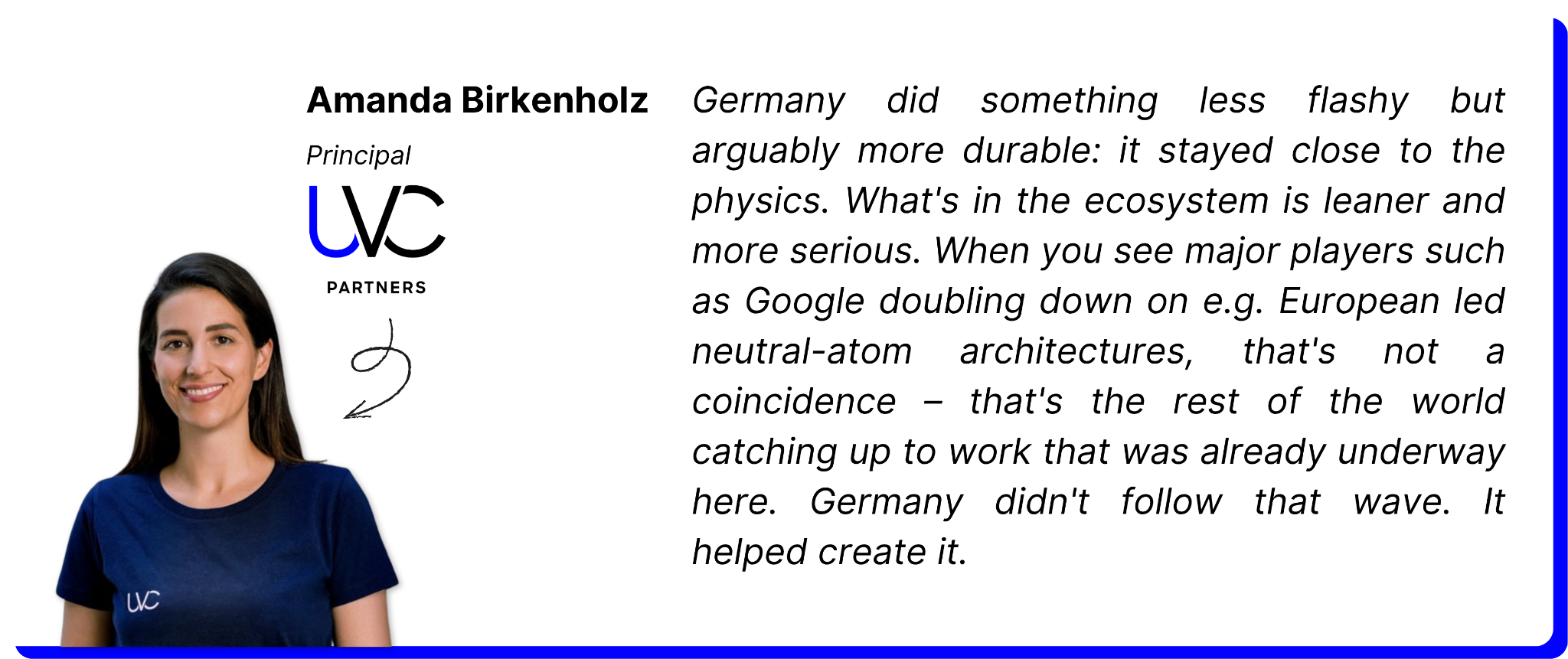

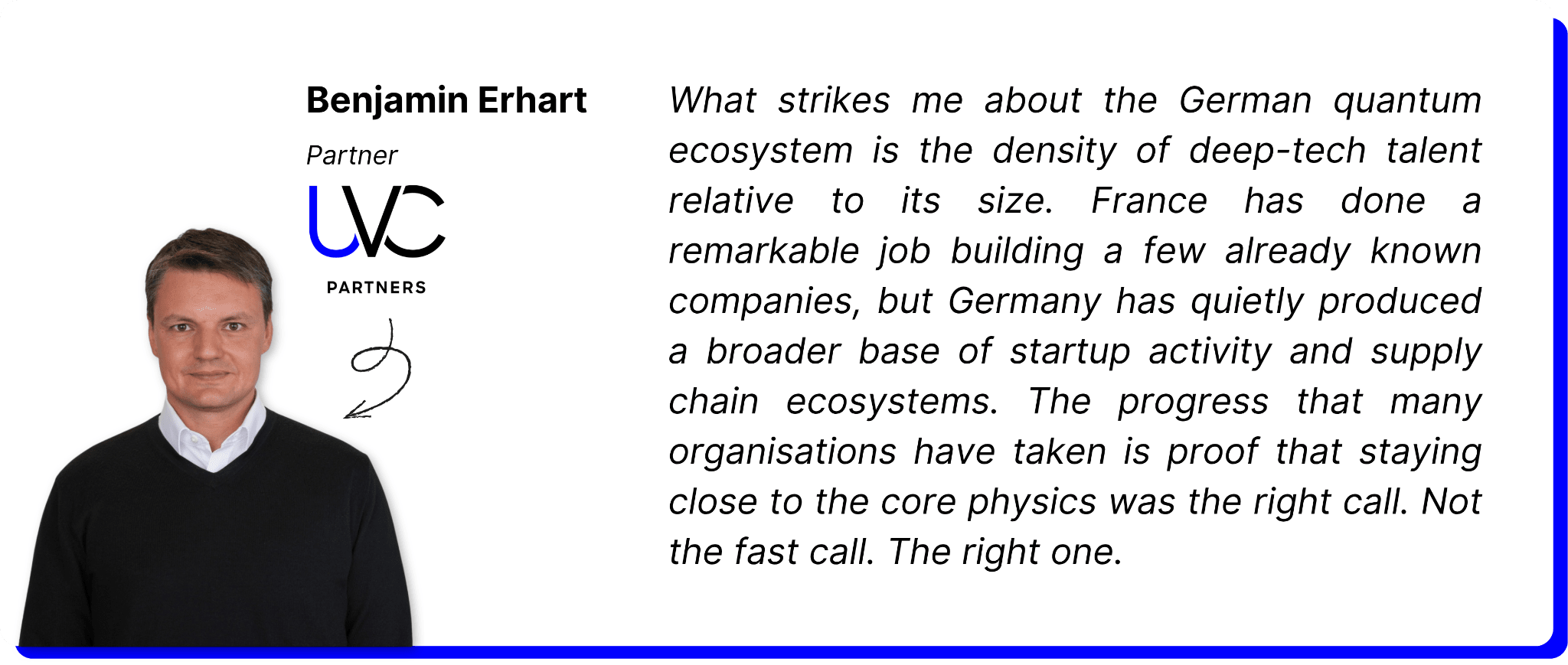

We identified 415 founders, concentrated around five hubs: Germany, the UK, France, the Netherlands, and Spain. Germany hosts the most founders, despite having raised less funding in 2025 ($3.2B according to Dealroom) than France or the UK. The German ecosystem is dense with startups like Planqc (€50M Series A), and the depth of its research base is contributing to its position.

And while France has concentrated capital around fewer, larger companies like Pasqal and Alice & Bob, Germany has spread it across a broader base of startups and supply chain companies.

It’s also no secret that Europe produces top researchers, and that translates into founding teams: 58% hold a degree in physics, quantum physics, quantum computing, quantum engineering, or a directly related field. Among them, 80% have a PhD. Out of the top five countries, France has the highest concentration of quantum-related academic backgrounds – like Christophe Jurczak, co-founder of Pasqal, who holds a PhD in quantum physics from École Polytechnique.

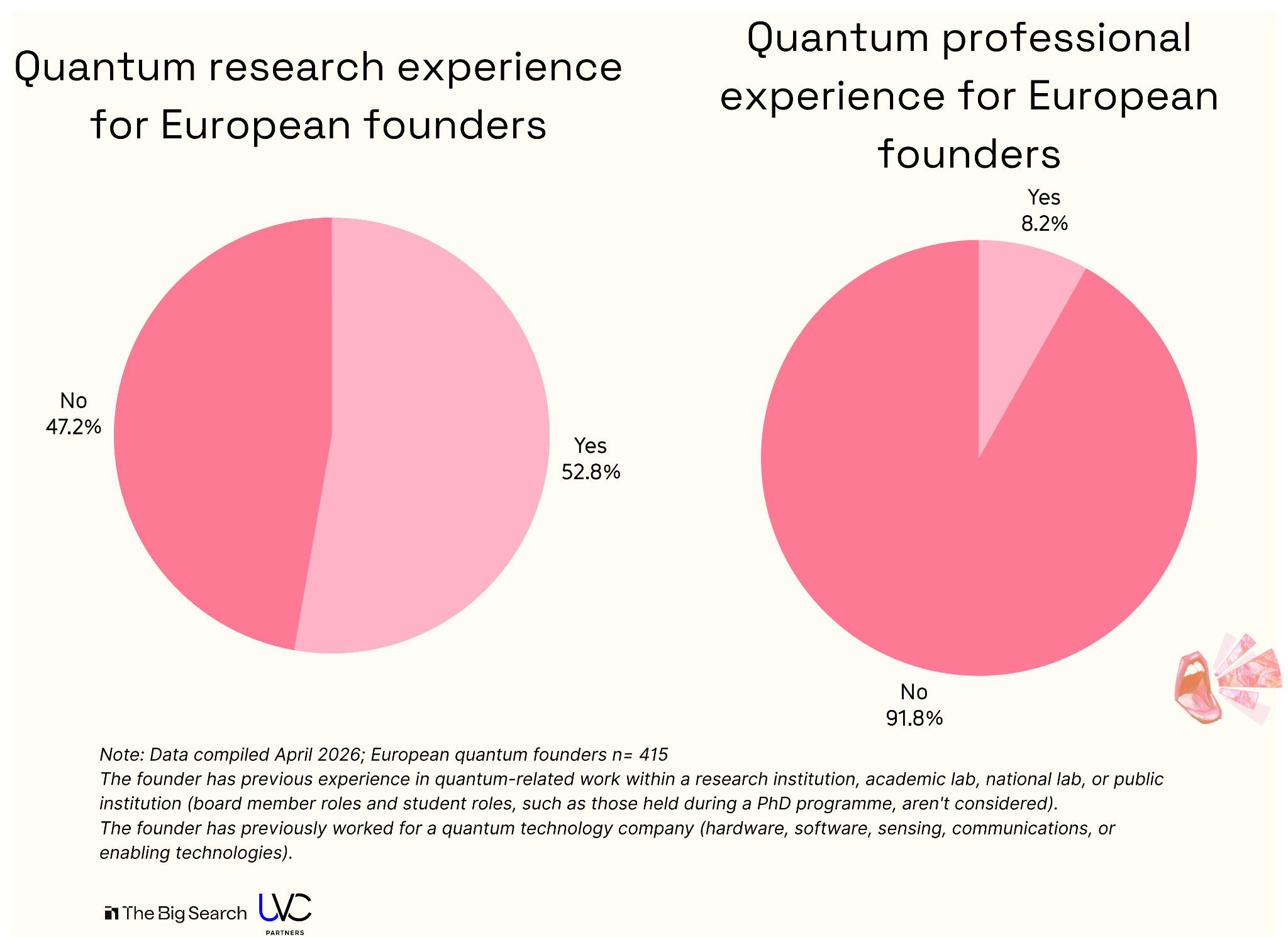

We also found that 52.8% have quantum experience through research institutions, academic labs, or public bodies. Most founders moved straight from academia/research to founding their company, often from national research labs like CNRS, QuTech, Max Planck Institutes, INFN, TNO, CSIC, or VTT. This is structurally different from the US, where company-to-company moves are more common.

The 8.2% who do have professional industry experience came from (1) a national lab’s commercial arm, (2) a quantum-adjacent company, or briefly (3) a top-tier strategy consultancy.

Quantum C-levels come from Big Tech

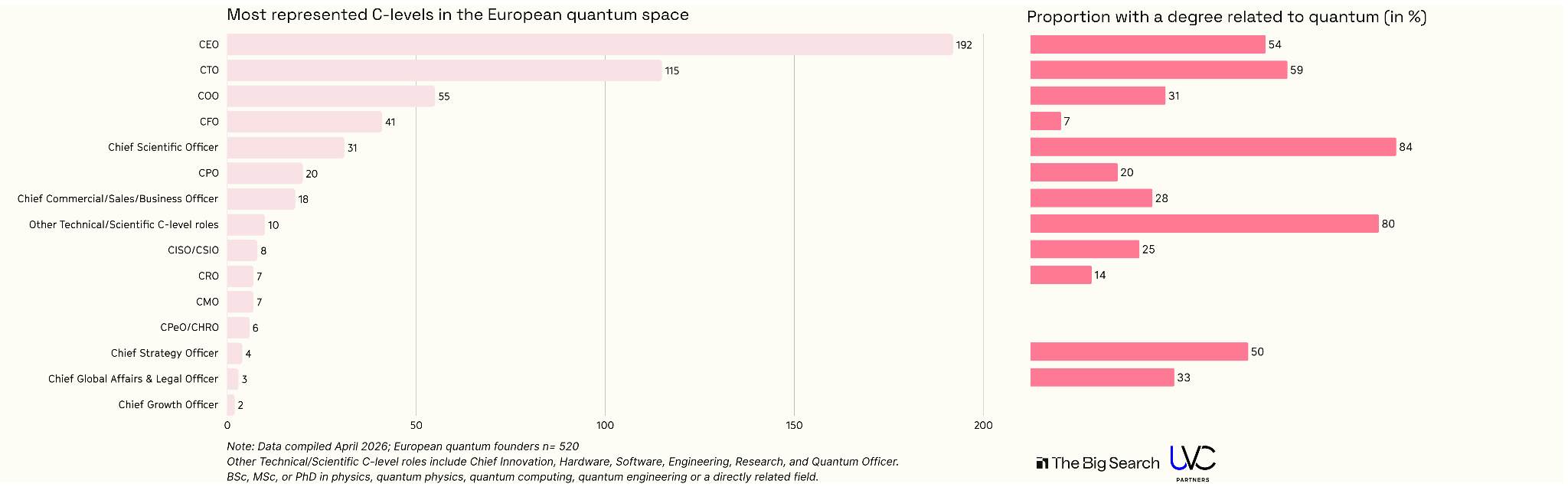

We mapped 520 current C-levels based in Europe. Unsurprisingly, CEOs, CTOs, and other scientific C-level roles are the most represented.

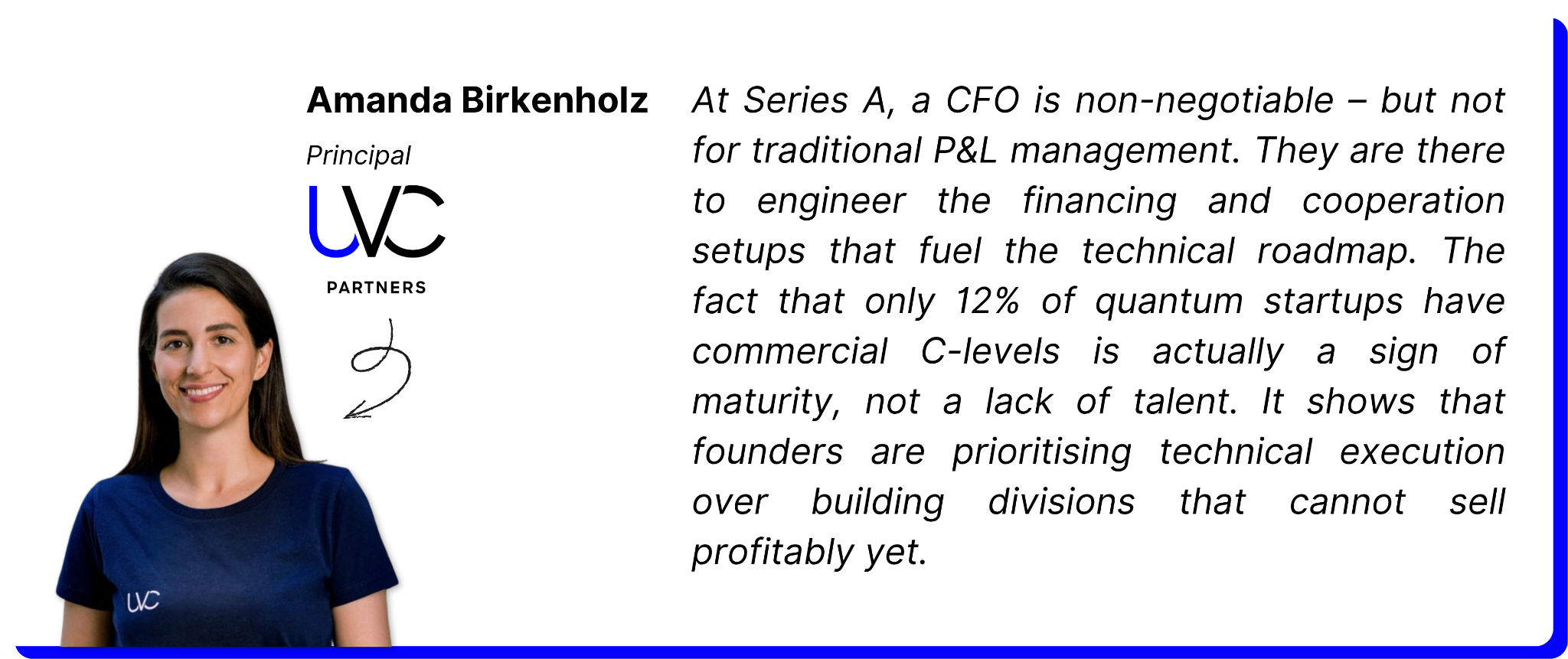

Among companies that have a CFO, 56% have raised at least a Series A. When most of your revenue is hypothetical, and your growth depends on fresh capital, having a CFO on board is essential. And because most companies are still early-stage, only 12% have a commercial C-level (Chief Growth Officer, CRO, CMO, or CCO/CSO) – we’ll come back to that in the next part.

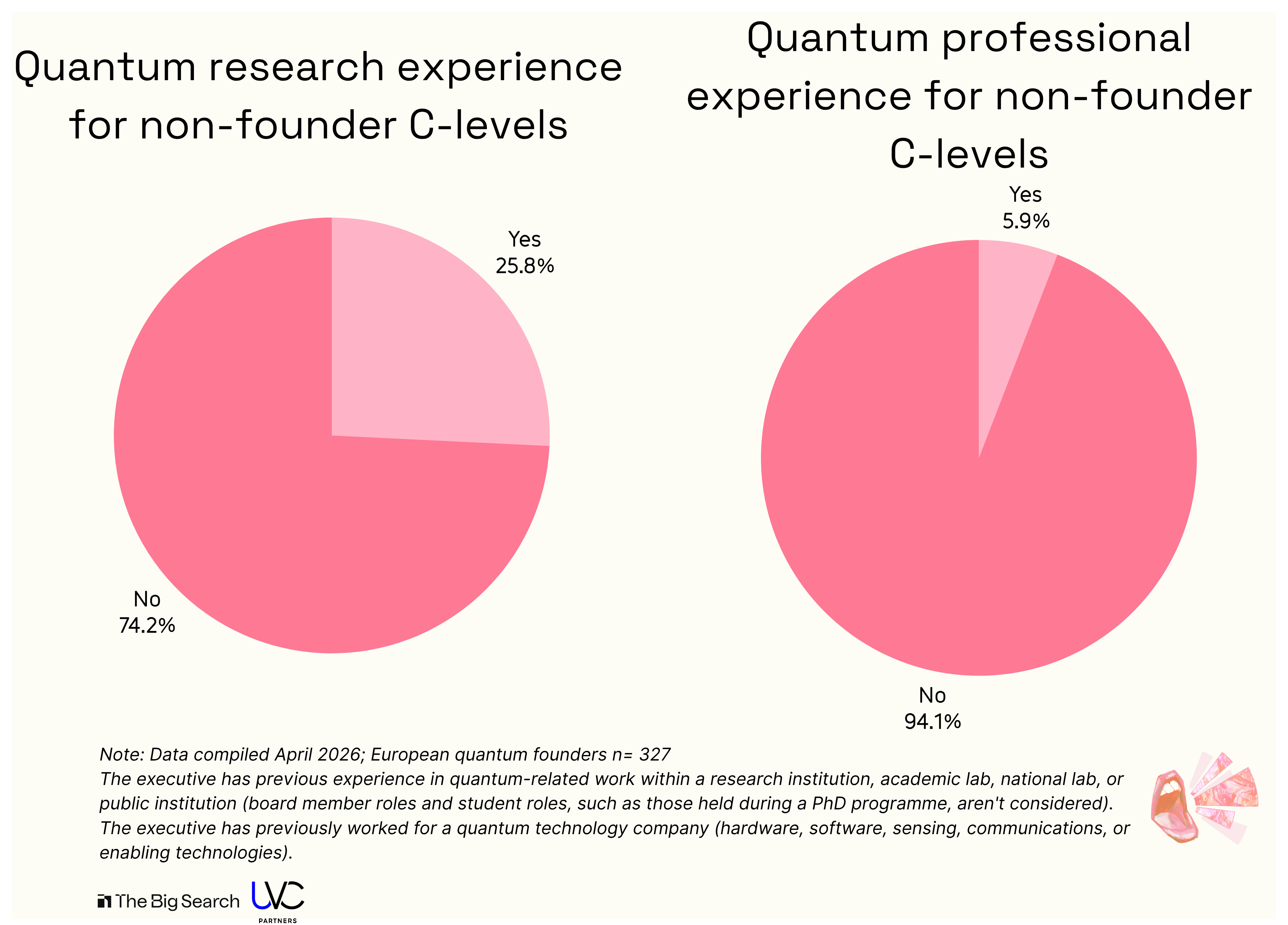

Among current C-levels, 193 are founders. That leaves 327 non-founder C-levels. As the data shows you, they have less research and industry experience than founders, and those who do are CEOs, CTOs, or Chief Science Officers.

One-fourth originates from Big Tech or large corporations. IBM and Microsoft, both industry leaders in quantum, are the most represented. Most held research or tech/engineering roles there, though we found a few commercial profiles: Xavier Pereira, Chief Growth Officer at Quandela, Robin Wittland, CCO at QuiX Quantum, Christian Georgeson, CMO at Arqit, and Jonathan Yates, CRO at Silent Waves.

For security-focused quantum companies like PQShield, ResQuant, Arqit, and CyberHive, their C-levels came from defence, government or space tech organisations - e.g. QinetiQ, UK MoD, Lockheed Martin, or Airbus.

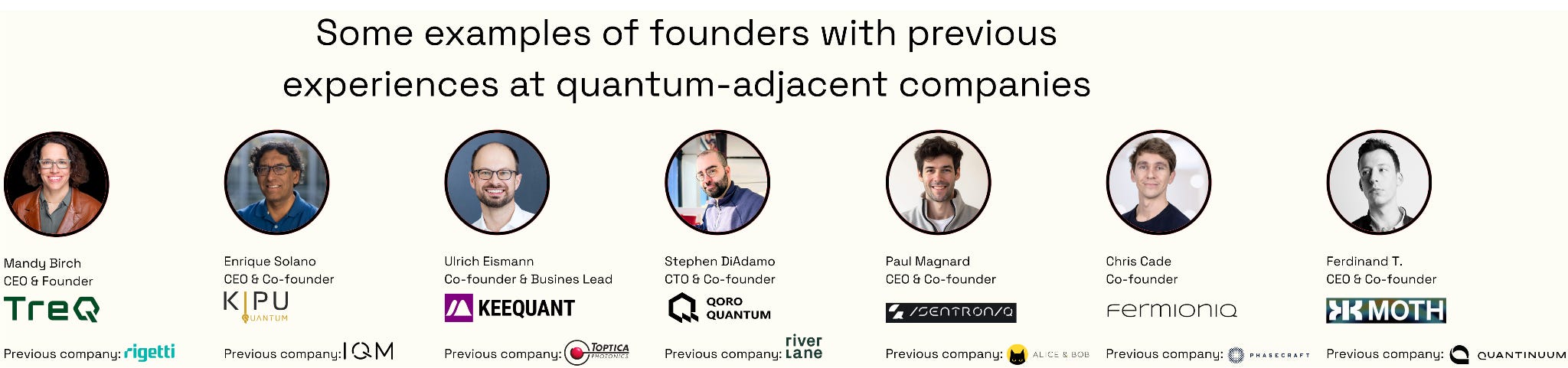

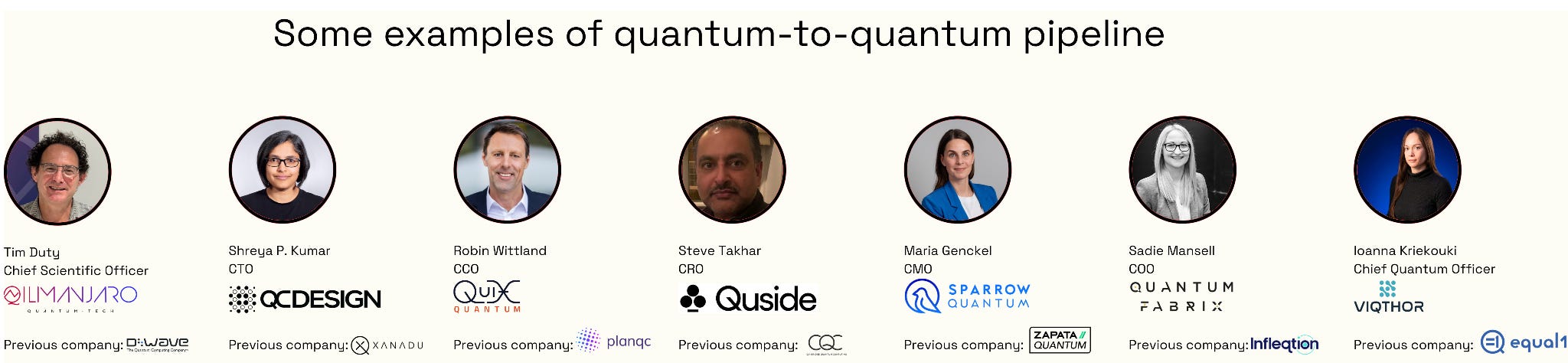

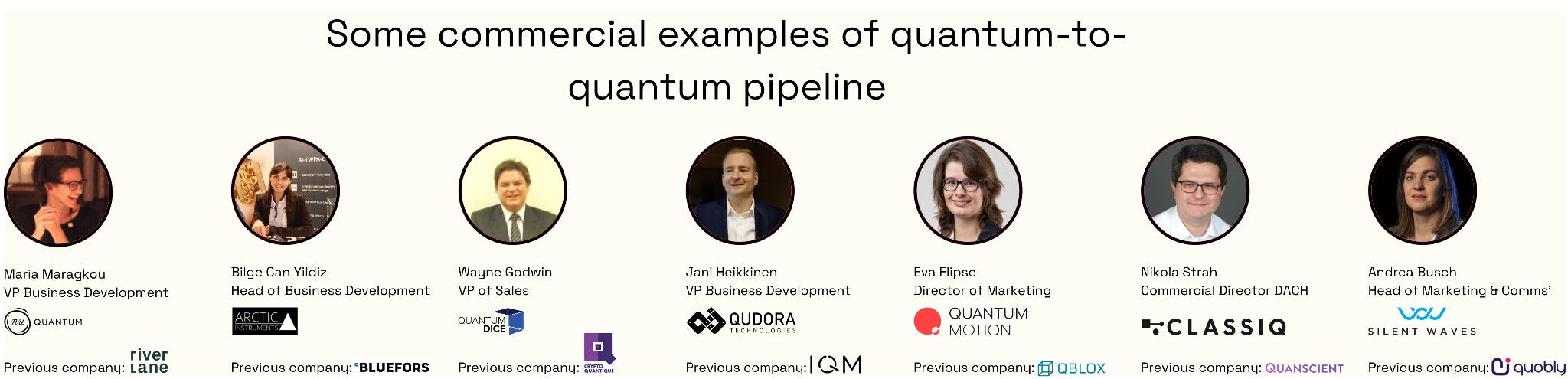

Finally, there is a small but emerging quantum-to-quantum pipeline (5.9%):

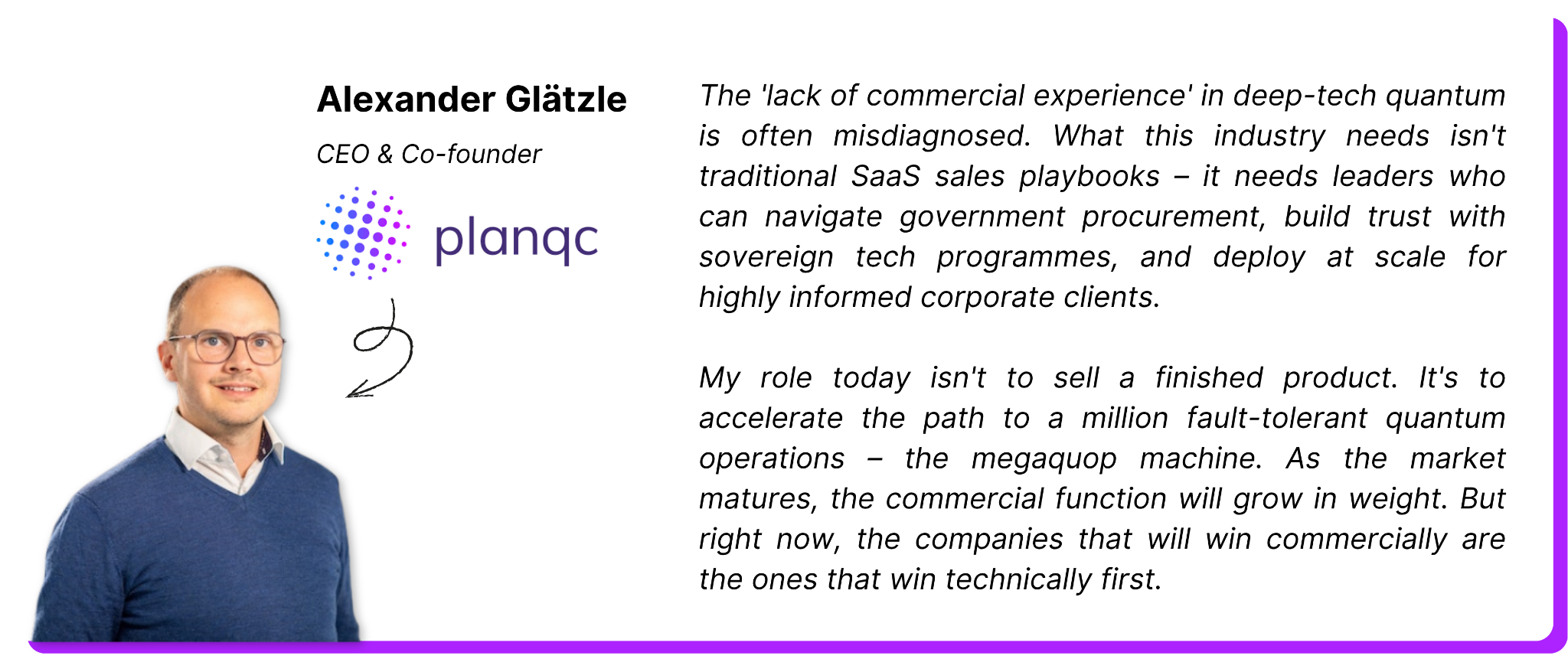

The European quantum ecosystem lacks commercial leadership

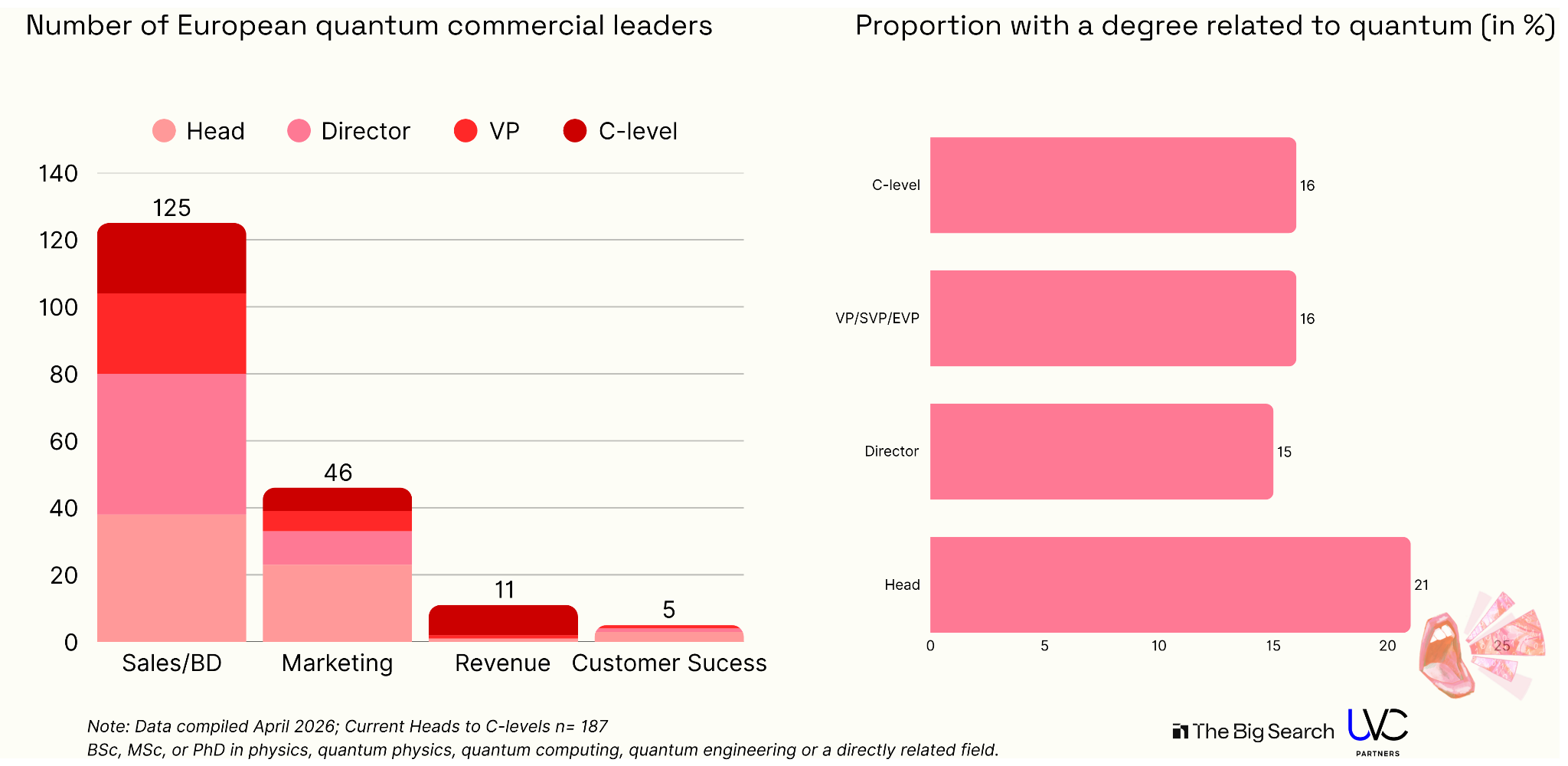

We tracked 187 current commercial leaders across 86 companies. That means only 36% of European quantum startups have at least one commercial leader in place, from Head to C-level. Unsurprisingly, they work for mature companies like IQM, Arqit, or Multiverse Computing, which have already generated revenue streams.

Nearly half are recent hires: 46% have a tenure of one year or less.

As more European quantum companies close Series B-C rounds (e.g. Quantum Motion or Quantware), they need commercial leaders who understand (1) government procurement, since much of the revenue comes from defence and national programmes: 27% have experience selling to governments or the public sector. And (2) technical credibility: 61.5% hold a STEM degree, though only 19% have one directly related to quantum.

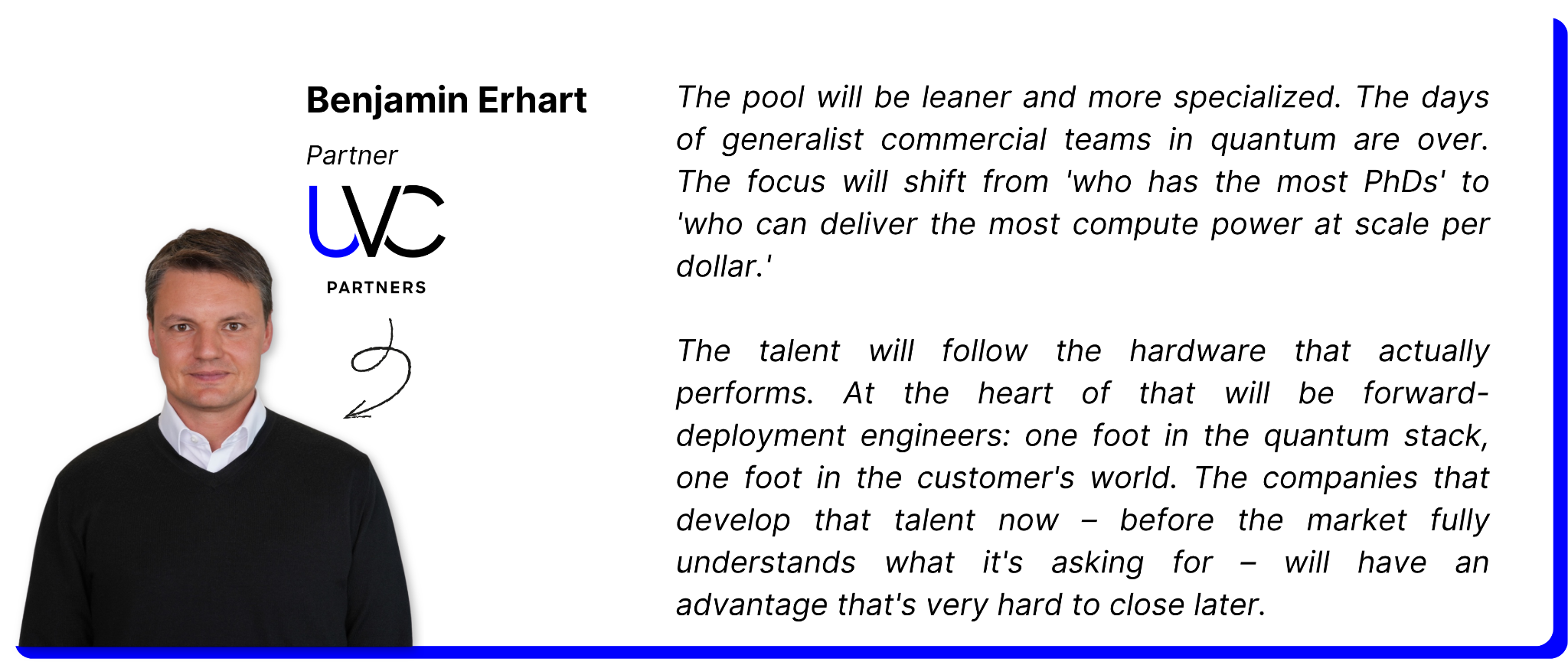

The hiring pipelines are similar to what we saw with C-levels: Big Tech and large corporates remain the most frequent sources; defence and space feed security-focused companies, and semiconductor experience flows into hardware-focused startups.

Some commercial leaders also previously worked at another quantum company (10%).

We’ve now mapped the backbone of European quantum: founders, C-levels, and commercial leaders. For now, the sector is shaped by academia, with public research labs acting as training grounds for most founding teams.

As more quantum startups close later VC rounds, demand for C-levels and commercial leaders who can sell to governments/public institutions and enterprises will increase.

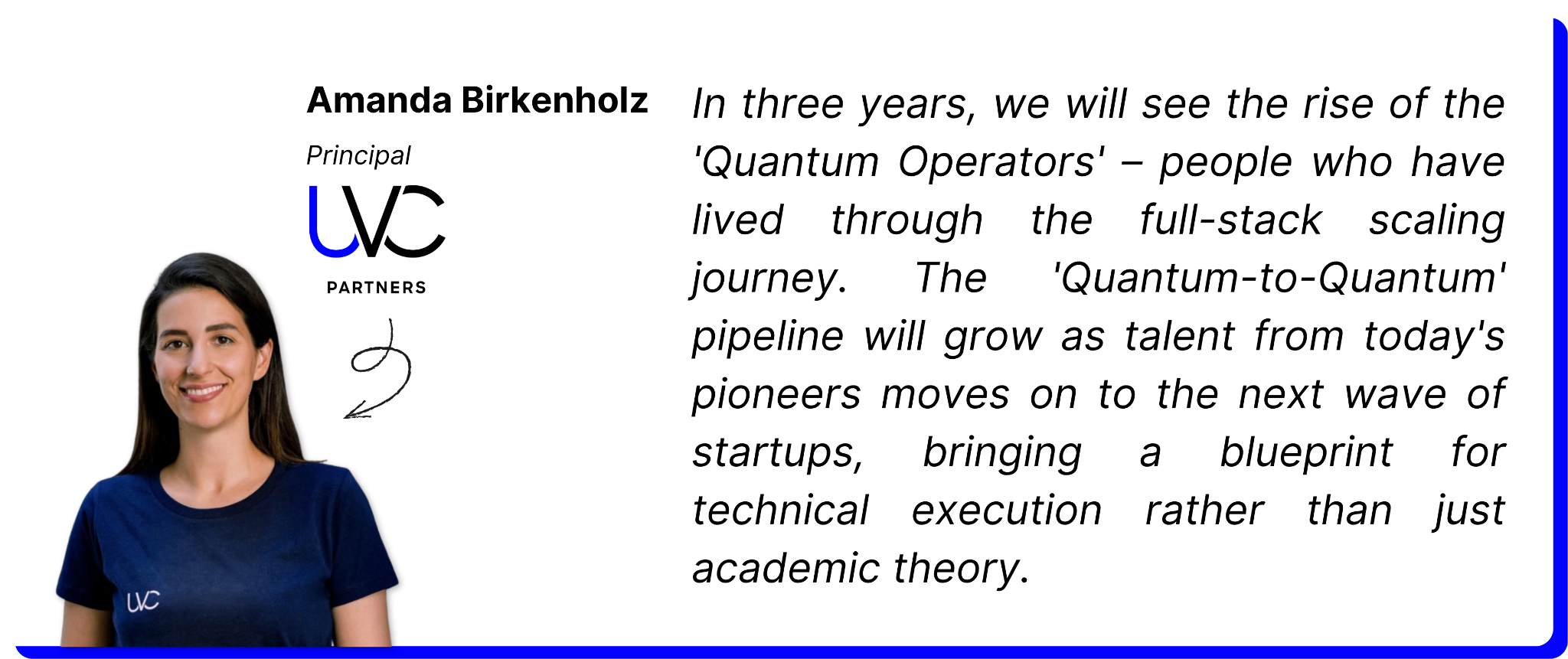

And when IQM, Pasqal, and Quantinuum go public, the quantum-to-quantum pipeline will likely get bigger. Early hires who cash out will launch their funds or move to smaller startups, bringing scaling experience with them.

Practical quantum computers may still be years from wide availability, but the talent groundwork is being laid now. The road ahead for quantum startups will likely involve continued advances in full-stack technology and more partnerships with corporates and public organisations to (1) drive early adoption, (2) create first market opportunities, and (3) generate tangible revenue streams.

Want to see how we can support your search? Visit our website to explore our services and learn what we can do for you.

100/100