Understanding Europe’s Quantum Technology Landscape Through IQM and Quantinuum's Talent Structures

The talent structures of IQM and Quantinuum show that the sector is shifting from scientific exploration to a mainstream industrial field with real-world applications.

Over the last few months, you’ve seen us dig into the European DeepTech ecosystem across energy, batteries, robotics, AI, and defence. Today, we’re exploring another field you’ve probably heard a lot about: quantum computing (the most exciting thing on the horizon, according to Google CEO Sundar Pichai).

Why now? Because quantum computing is on the verge of unlocking major advances across industries, and the global race is on. Leading countries are pouring billions into quantum technologies, each aiming to secure an edge in the “quantum revolution.” Europe has also set its sights on becoming the first continent to reach the critical threshold of qubits for solving real-world problems by 2035.

And what better way to understand the European landscape than through the lens of two leading European unicorns that each closed huge September funding rounds?

IQM, the Finnish company founded in 2018 by Jan Goetz, Juha Vartiainen, Mikko Möttönen, and Kuan Yen Tan, raised $320M at Series B.

Quantinuum, formed in 2021 from the merger of Cambridge Quantum Computing (initially founded by Ilyas Khan) and Honeywell Quantum Solutions, raised a $600 million Late VC round.

We looked at their talent structures from Lead to C-level, identifying 74 professionals at IQM and 119 at Quantinuum1. Across both companies, women represent ~23% of leaders, which is relatively strong in a traditionally male-dominated DeepTech space.

Now, let’s dive into their composition and see what their teams can tell us.

How IQM and Quantinuum’s talent composition has evolved over the years

IQM’s hiring really took off after its Series A in November 2020, driving a strong growth wave between 2021 and 2023. Quantinuum ramped up recruitment after the 2021 merger.

Both companies, however, show a noticeable uptick in departures in 2024. So, what’s behind that?

Well, the 2024 drop isn’t a sign of a decline in demand for quantum. Both IQM and Quantinuum actually restructured and shifted focus from “grow fast” to “prove commercial viability.”

In fact, the same year, IQM signed an agreement with EuroHPC to deliver two quantum computers. At the same time, Quantinuum announced a breakthrough in logical quantum computing, marking a shift from scientific exploration to large-scale engineering. Proof that the sector is still moving forward, just more strategically. The goal is now to turn quantum research from a niche academic pursuit into a mainstream industrial sector.

You can actually see it in this graph: 2024 was a retooling year for IQM, marked by a restructuring program to prepare for its next phase of growth. That restructuring, combined with a pause to digest the rapid 2023 expansion, likely explains why departures outpaced new hires in 2024.

On the other hand, Quantinuum’s 2024 spike aligns with the typical post-merger churn pattern, which often occurs one to three years after integration, as retention grants expire and consolidation efforts wind down. Yet, it didn’t stop the company from continuing to expand its team. With Honeywell as its major shareholder and a $300 million equity round led by the company, Quantinuum had the backing to scale while others were tightening up.

But this also highlights a broader issue: Europe still struggles to attract enough private quantum investment. That gap increases the risk of European startups being acquired by non-European corporates, potentially leading to losses of critical technologies, technological sovereignty, and talent.

How IQM and Quantinuum structure their teams

Both IQM and Quantinuum have built strong technical and engineering teams to develop and refine their products. It shows the reality of building quantum systems capable of reaching computational power that no binary-based device could ever achieve.

We’re now seeing real-world applications emerge in secure communications, critical infrastructure, and healthcare data protection, and that’s exactly where IQM and Quantinuum are gaining commercial traction.

To do so, both companies have been rapidly scaling their commercial teams: 80% of IQM’s commercial hires and two-thirds of Quantinuum’s joined since 2023. Today, the commercial function is the second-largest one at IQM and the third-largest one at Quantinuum.

It may still take a few more years before practical quantum computers are widely available, but the direction is clear. The road ahead for IQM and Quantinuum will likely involve continued advancements in their full-stack technology and more strategic partnerships with corporates and public organisations to (1) drive early adoption, (2) create first market opportunities, and (3) generate tangible revenue streams.

C-level breakdown: IQM and Quantinuum

To build on the point above, both companies have brought in Chief Commercial Officers within the past two years. In February 2024, IQM even moved to a co-CEO structure, appointing Mikko Välimäki to focus on enterprise commercial operations. It’s a smart move, especially given that Europe still lacks major industrial early adopters of quantum technology and, thus, a strong pipeline of customers and collaborators that can accelerate product development. This can deprive emerging actors of clear market opportunities, making dedicated commercial C-levels essential to drive adoption.

They’ve also made sure to have people leading Legal and Public Affairs. This is essential when you’re working with governments, public institutions, and defence partners. Another interesting signal? Both companies have CFOs with serious IPO credentials. It’s hard not to wonder if an IPO could be somewhere on the horizon.

Neither company, however, has a CTO. Since they develop entire quantum systems and have multiple technical layers, they’ve spread leadership across specialised technical and scientific roles. At IQM, three VPs oversee the quantum divisions. Quantinuum, on the other hand, has an “army of science” led by three Chief Scientists, alongside a Chief Product Officer and several distinguished engineers. This configuration tells customers “we ship product and do research” without relying on a single person to own every scientific and engineering decision.

Where IQM and Quantinuum’s talent is located

While Quantinuum has a strong UK footprint, most of its talent is still based in the US. A decision that comes with its reasons. Contrary to Europe, which may lack the right talent who’ve already taken DeepTech companies from Series B to late-stage success, the US represents the best place to scale and tap into a larger pool of experienced DeepTech professionals. Just think of IonQ, a public quantum company that has secured contracts with universities and defence research labs.

IQM, on the other hand, positions itself as Europe’s clear quantum champion to achieve the continent’s industrial competitiveness and technological sovereignty. Yet, its recent backing from Ten Eleven Ventures marks IQM’s first US investment and comes at a key moment as the company starts expanding internationally.

Both companies are eyeing Asia. IQM has a presence in South Korea and Singapore, while Quantinuum operates in Japan and partners with Mitsui to co-develop products and expand its market reach.

And let’s not forget Asia dominates semiconductor manufacturing with unmatched precision, especially in high-end nodes, which are considered an art form. Since semiconductors and quantum are deeply connected (semiconductor theory literally stems from quantum mechanics), it’s no surprise that both IQM and Quantinuum see massive potential there.

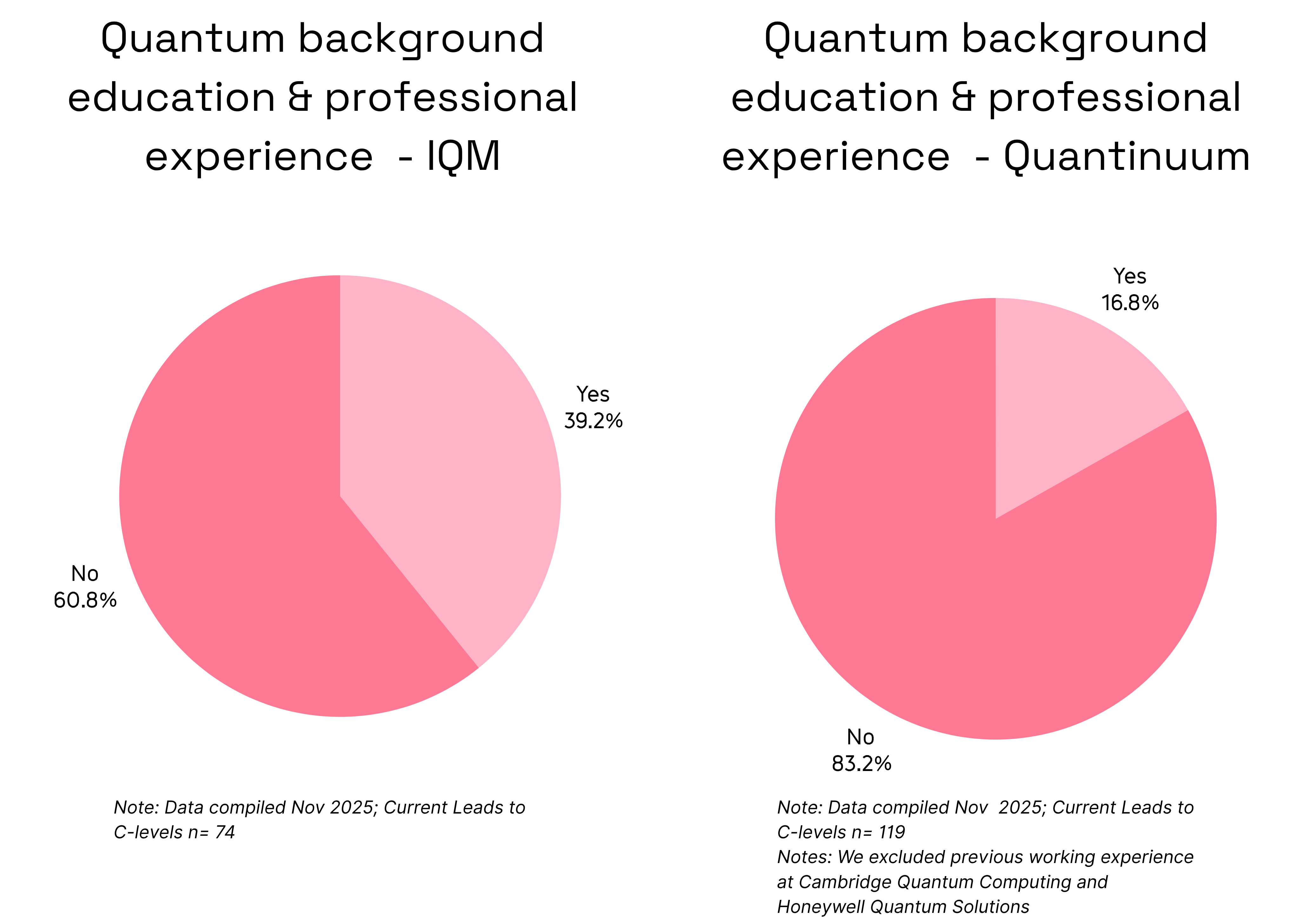

Do they have quantum experience?

IQM has about 2.3x more talent with a quantum background - meaning they’ve either studied quantum or worked at a quantum company - compared to Quantinuum. Still, overall, that absolute number isn’t huge. It suggests the European quantum ecosystem continues to source much of its talent from outside the field.

Most of them come from corporate or academic backgrounds. At IQM, companies like Nokia, Microsoft, and ABB appear frequently in career histories. At Quantinuum, many come from Honeywell and its subsidiaries, such as Honeywell Aerospace. There is also a notable presence of talent from defence primes like Lockheed Martin, reinforcing Quantum’s potential as a dual-use technology and attracting professionals with experience in defence and public security.

According to a McKinsey report, Europe has the world’s highest concentration of quantum technology talent, thanks to universities launching new master’s programs in quantum and a growing base of +160 VC-backed quantum startups. Yet, the supply still falls short. The reason is that most experienced quantum professionals are already employed by leading startups that dominate the European landscape, making it increasingly difficult and costly to attract them.

This talent bottleneck undermines Europe’s ability to build critical mass and scale, slowing down the commercialisation pipeline and limiting the development of a globally competitive European quantum industry.

Conclusion: The state of Europe’s quantum ecosystem

The talent structures of IQM and Quantinuum, along with recent developments around both companies, show that the sector is shifting from scientific exploration to a mainstream industrial field with real-world applications.

But as quantum hardware matures and software frameworks become more robust, companies now need deeper financial backing and stronger talent pools to move from proof of concept to commercial viability.

The good news is that investors are beginning to respond. 55 North recently closed the first round of a €300 million fund dedicated to quantum ventures signalling a turning point. This is only with this kind of support that Europe will build the backbone of its quantum industry and develop a strong talent pipeline.

Quantinuum was formed through the merger of Honeywell Quantum Solutions, focused on hardware, and Cambridge Quantum, known for its work in algorithms, chemistry, and cybersecurity. As a full-stack company, Quantinuum supports both cutting-edge ion-trap hardware and multiple software lines of business. This structure results in a higher concentration of pure scientists, physicists, and R&D roles compared to a hardware-deployment-driven builder like IQM. For this reason, we excluded Quantinuum from our analysis to create a more balanced comparison between the two companies.