European Defence Tech 2025: The Talent Lens, by The Big Search x Dealroom

We’ve mapped the backbone of European defence tech: founders, C-levels, commercial leaders, and the investors behind them.

We partnered with Dealroom and Resilience Media to build the 2025 European Defence Tech Report. As part of that work, we conducted four focused talent mappings:

(1) European defence founders,

(2) Defence C-level executives,

(3) Defence commercial leaders from Head- to C-level,

(4) Defence-focused investors across both generalist and specialist funds.

In total, we mapped +4.000 professionals across 624 European defence tech companies and 82 funds active in this sector1. The full report is on Dealroom, but here you’ll find the key insights from our talent analysis.

As you already know, the sector has clear momentum. VC investment in European defence and defence-application tech startups is projected to reach $2.3 billion by the end of 2025, up 130% versus 2024. The market has grown considerably over the past few months/years, attracting more and more talent, founders, and investors. Yet it’s still a relatively new space in VC, with a fresh cohort of companies scaling fast, which makes a talent-first view of the landscape particularly interesting.

So, time to launch into the findings.

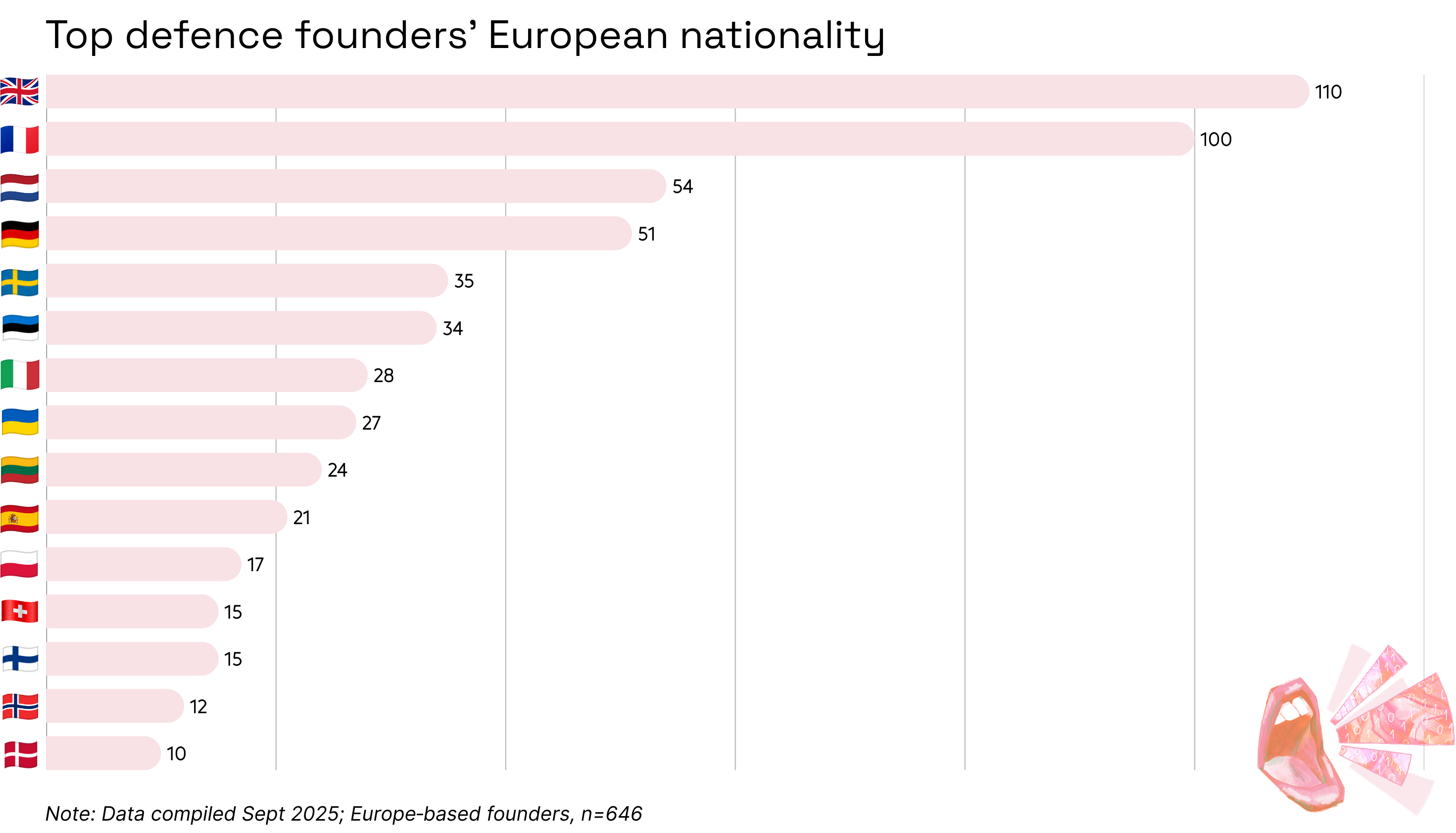

Who are Europe’s defence tech founders?

For our first mapping, we started right at the beginning of the defence talent pipeline: the founders. We identified 646 of them in total. As you’d probably expect, the vast majority are Europeans (95.6%). What stands out, however, is that Germany ranks below France and the Netherlands.

We can connect this to national defense investment. France tends to put most of its procurement money into domestic companies, framing it as strategic autonomy. The Netherlands shows a similar pattern in its maritime and radar programs, which often benefit Dutch firms. Germany, by contrast, has until recently directed a larger share of its spending toward external suppliers rather than its own industry. This difference has created more opportunities for defense tech founders in France and the Netherlands, where local demand supports new companies, than in Germany.

Among non-European founders, 32% come from NATO countries - Turkey, the US, and Canada - while 25% are from India. This likely ties to India’s strong STEM pipeline: each year, large numbers of Indian engineers and researchers move to Europe to study at top technical institutes, and many decide to stay and build their careers here.

We also found that 22% of founders are Eastern European, particularly from Estonia, Lithuania, and Ukraine. If you think about the region’s proximity to Russia and the heightened security risks, there - plus the ongoing war in Ukraine - it makes sense that defence innovation and entrepreneurship would be accelerating there.

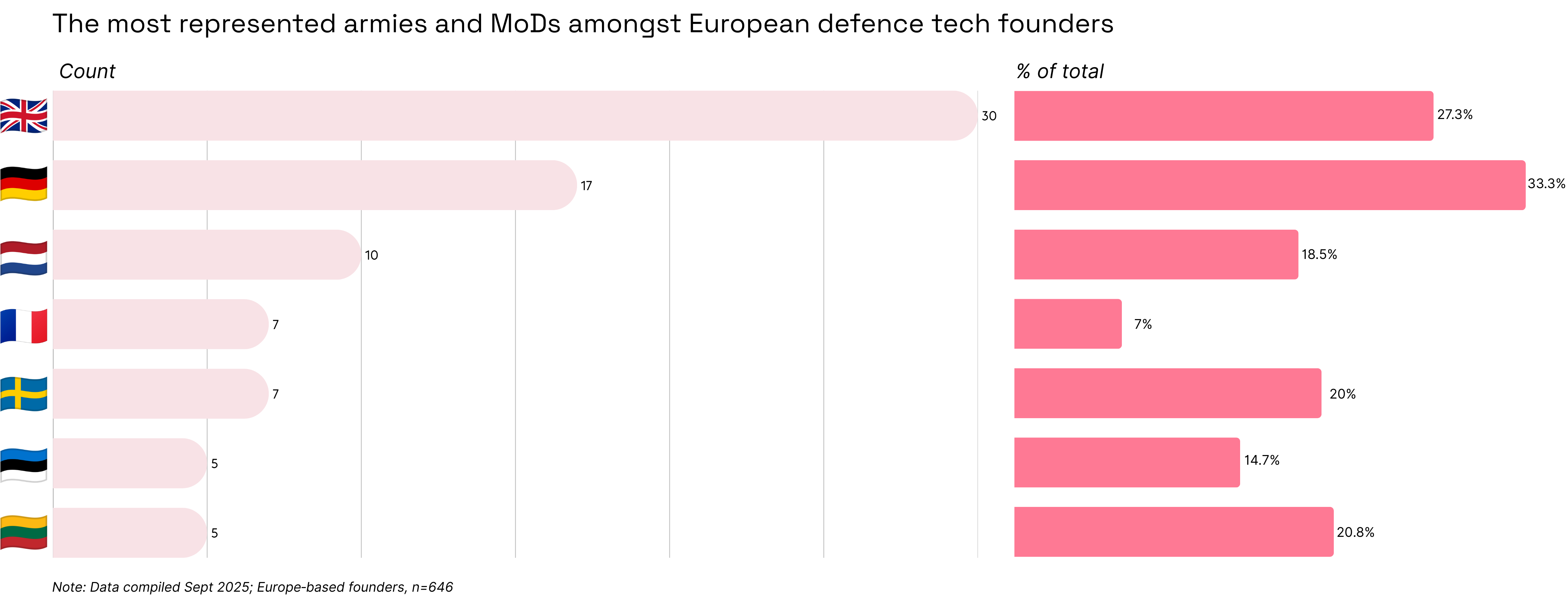

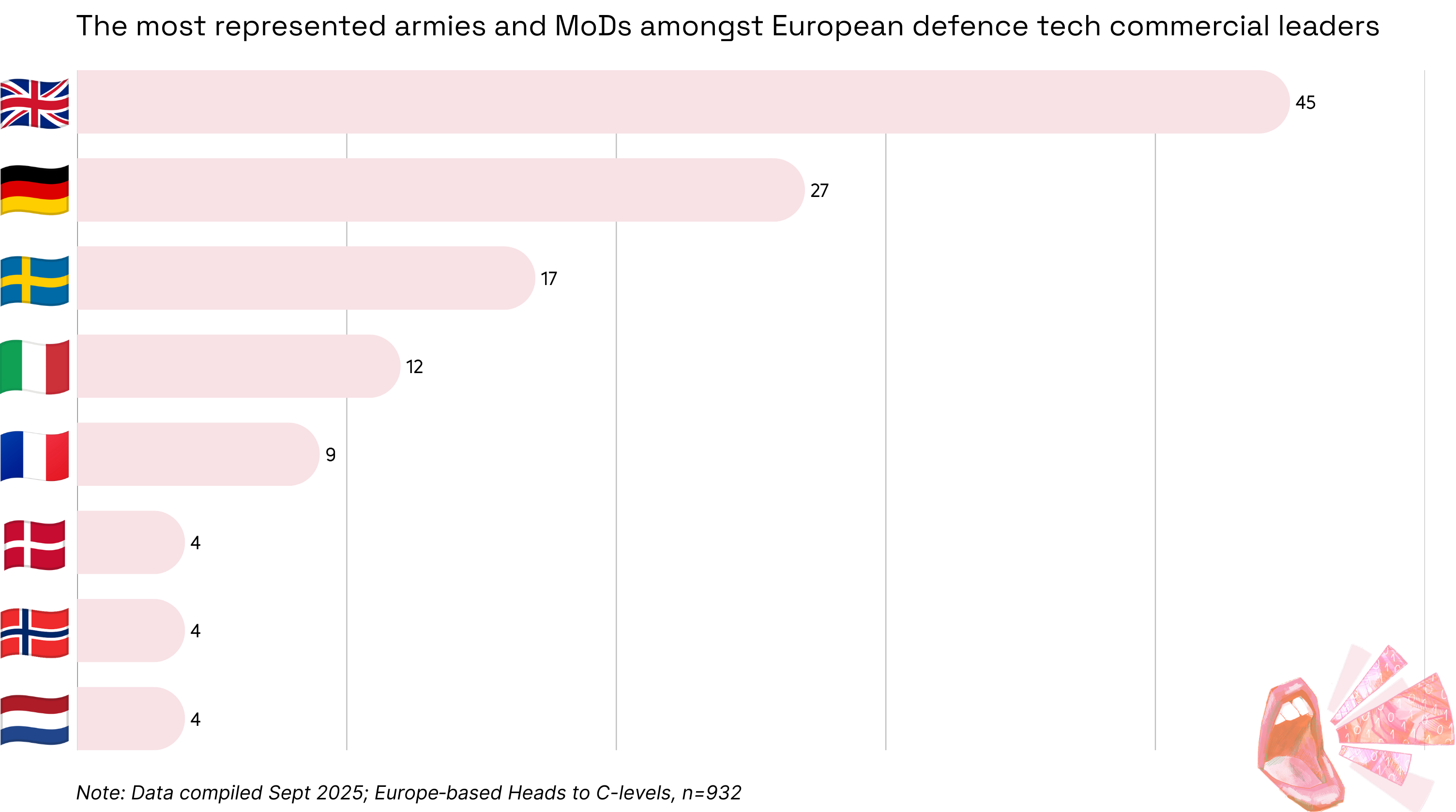

On top of that, 14.2% have an army or defence ministry background. Interestingly, while France counts many defence founders, only a small share has such experience. By contrast, in Germany and the United Kingdom, the Bundeswehr and HM Forces appear frequently, which points to clearer institutional pathways that help military talent transition into founding roles.

How many defence tech C-levels are there?

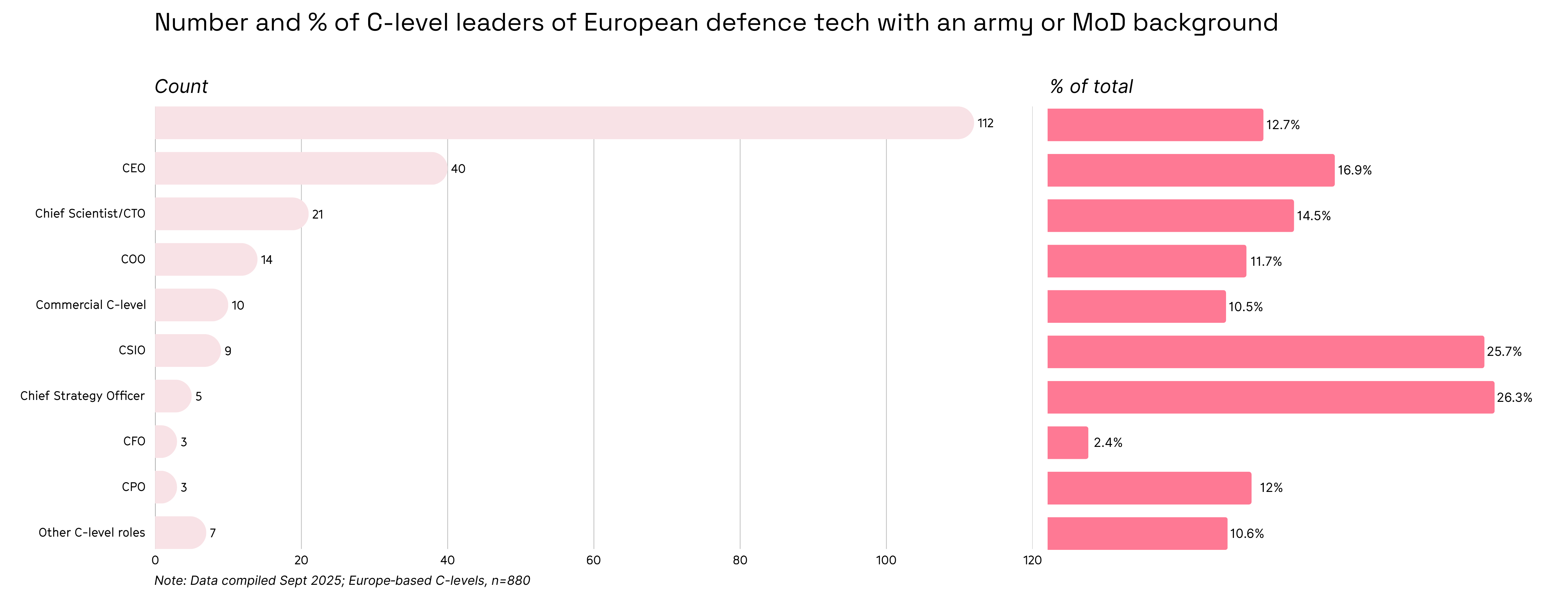

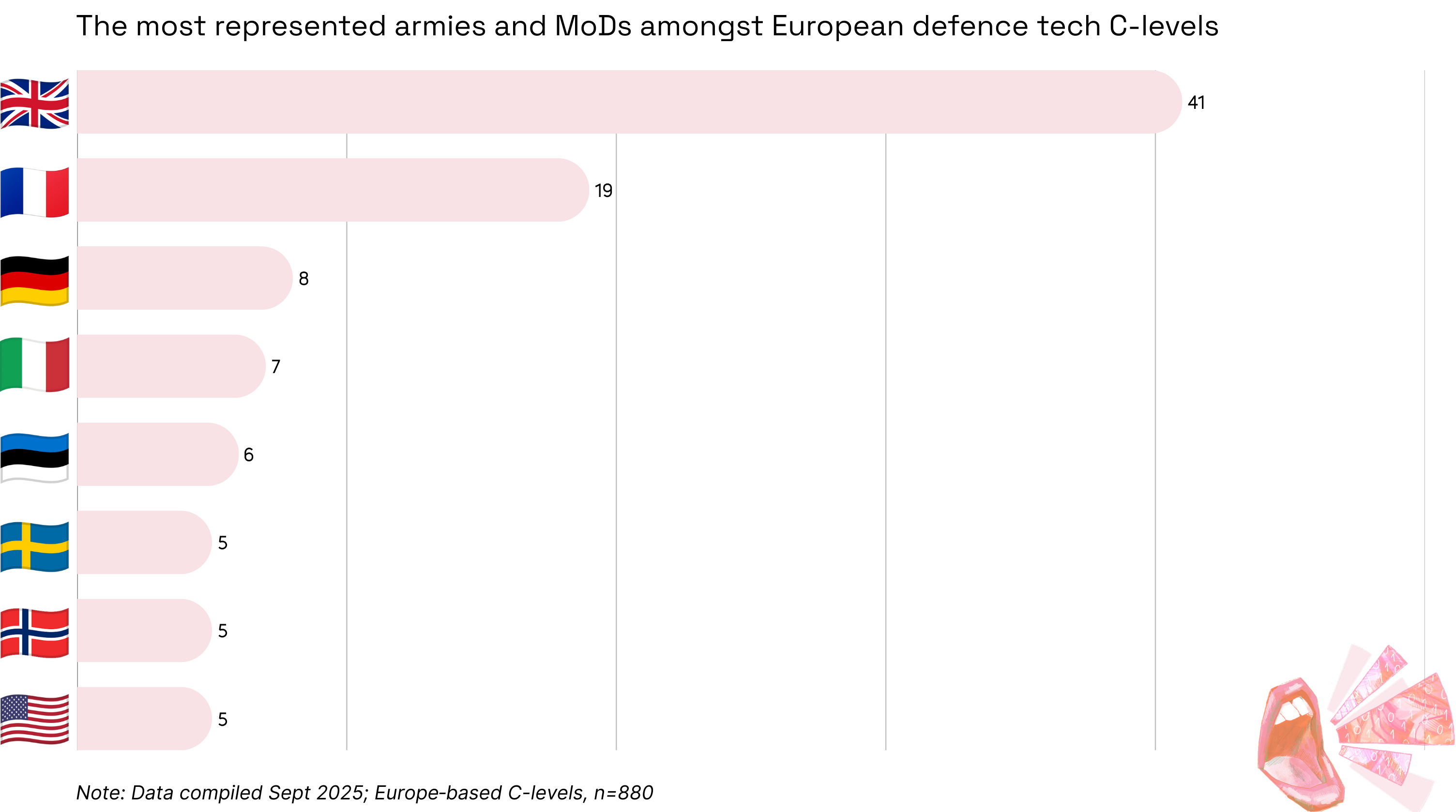

For our second mapping, we looked at the people making decisions inside defence tech companies: the C-level leaders. We identified 880 C-level executives, and 12.7% of them have an army or defence ministry background. It gives us 75 companies that have at least one C-level leader with direct military or MoD experience.

The roles with the highest share are Chief Information & Security Officer and Chief Strategy Officer. And it’s coherent: these positions demand security expertise, system know-how, familiarity with classified material, and a deep understanding of clearances, procurement, and export pathways. That naturally drives leaders who’ve spent time inside the forces.

Then, if you’re looking at CEOs, a service background brings credibility with end-users, stronger empathy for operational needs, and fluency in procurement. On the technical and product side, leaders with such experience can better identify product gaps and adapt solutions to military requirements.

By contrast, finance is the most transferable C-suite function. Since it rarely requires classified access, clearance isn’t a barrier - which is why you’ll mostly find civilian talent filling that function.

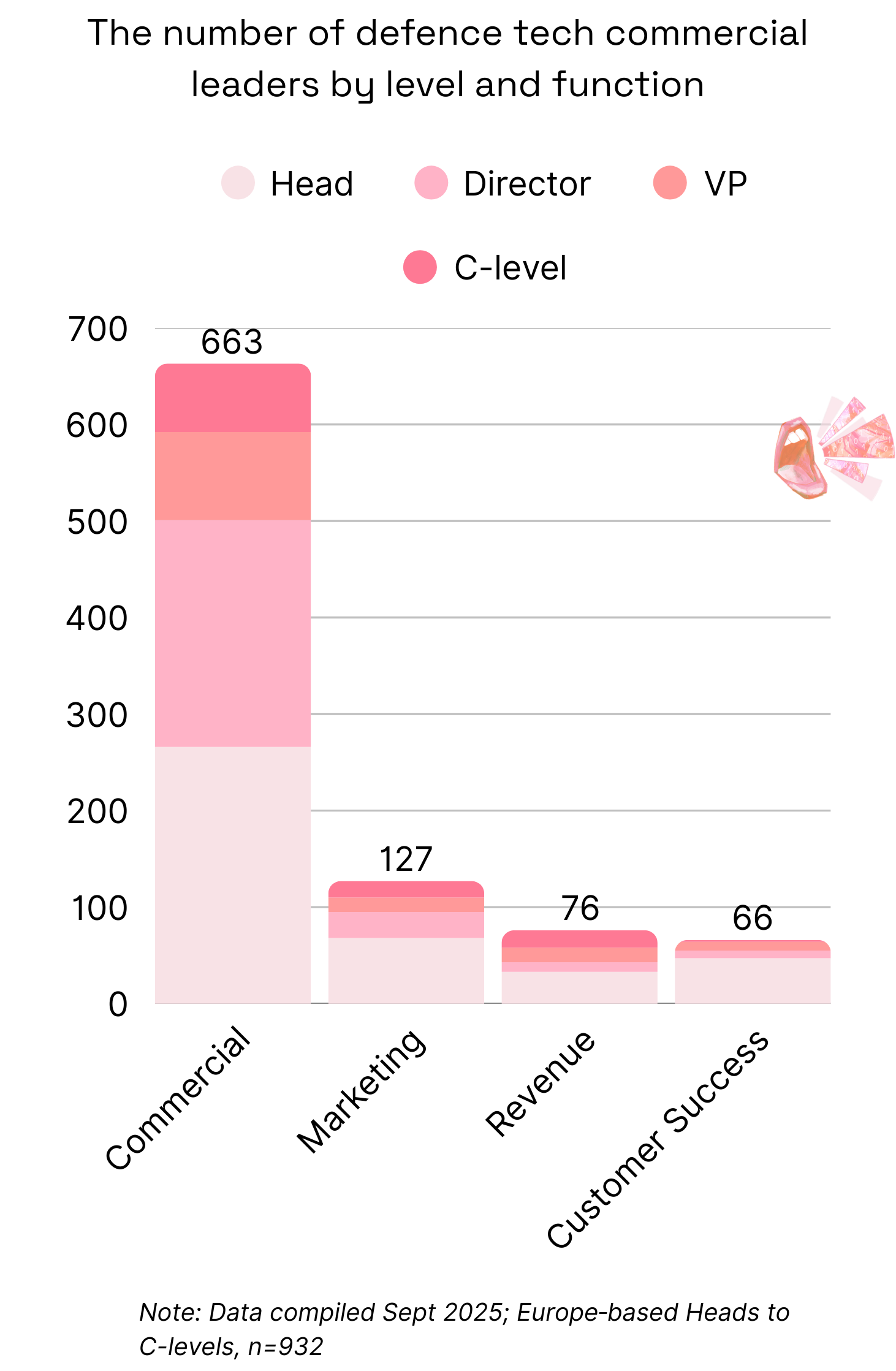

Why commercial leaders matter in defence

For our third mapping, we looked at the people on the frontline with defence customers - the ones chasing deals, closing them, and onboarding clients: the commercial leaders. In total, we identified 932 of them from Head- to C-level.

About a third of companies have at least one commercial leader, and about half of those already have someone at C-level. The rest cap their commercial functions at the Director or Head level, which makes sense for a young sector. But you can expect that to change fast. As the market gains maturity and more companies raise VC funding and move into scale-up mode, you’ll see more commercial leaders and C-levels getting appointed.

Sales, Commercial, and Business Development largely dominate. These companies need to generate revenue, and that requires someone who can navigate the long, complex public-sector sales cycles.

And it’s only once you start delivering at scale that you bring in Marketing, Customer Success, and Revenue leaders to educate and build trust, focus on long-term customer outcomes, or oversee the entire revenue engine.

Out of the 932 commercial leaders we identified, 130 have a defence or MoD background, which represents 13.9%. On the commercial side, selling to defence customers demands leaders who speak the same language as your buyers and understand the tech they need. That’s why 86.2% of leaders with such a background sit in Commercial, Sales, and Business Development roles.

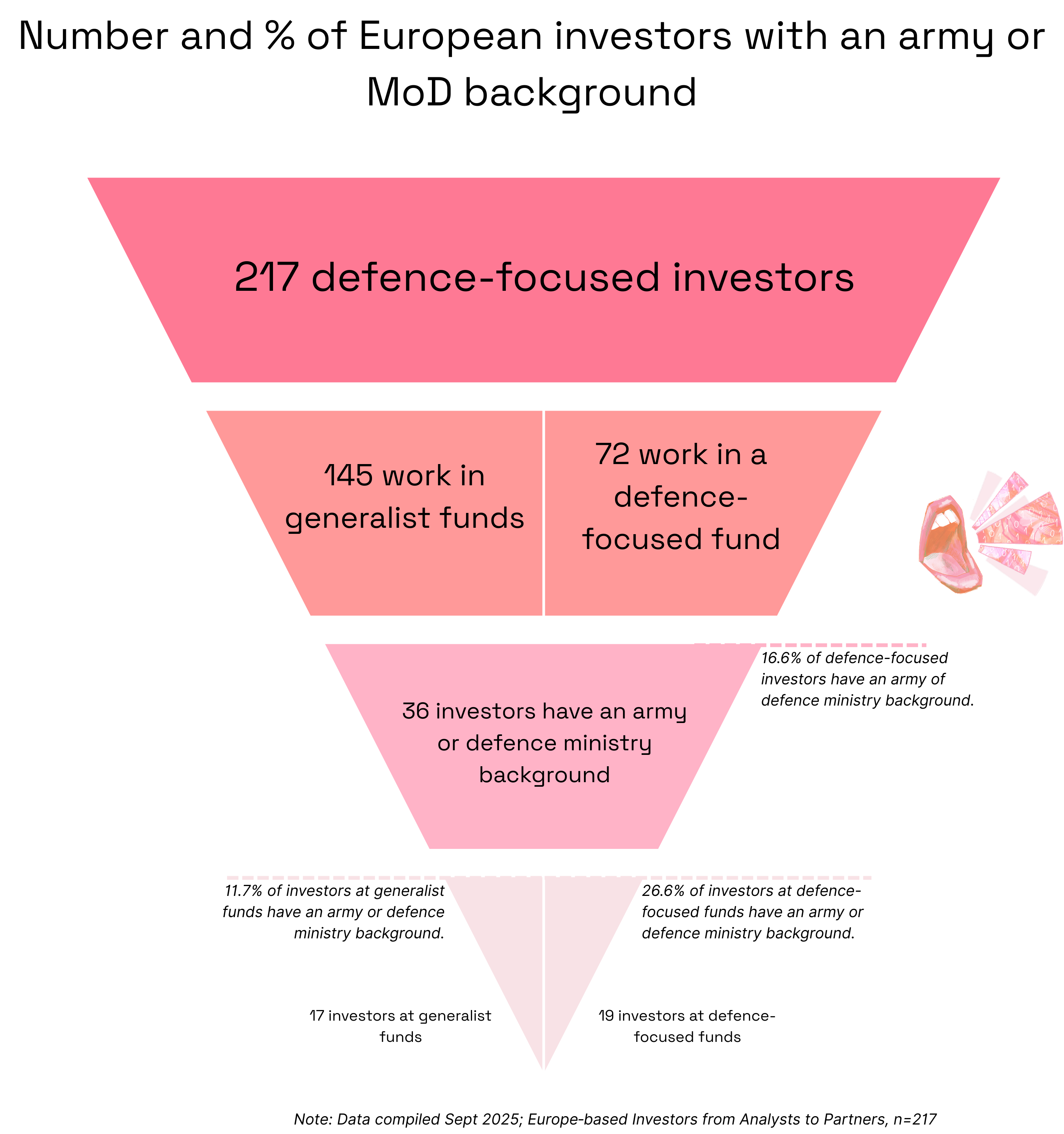

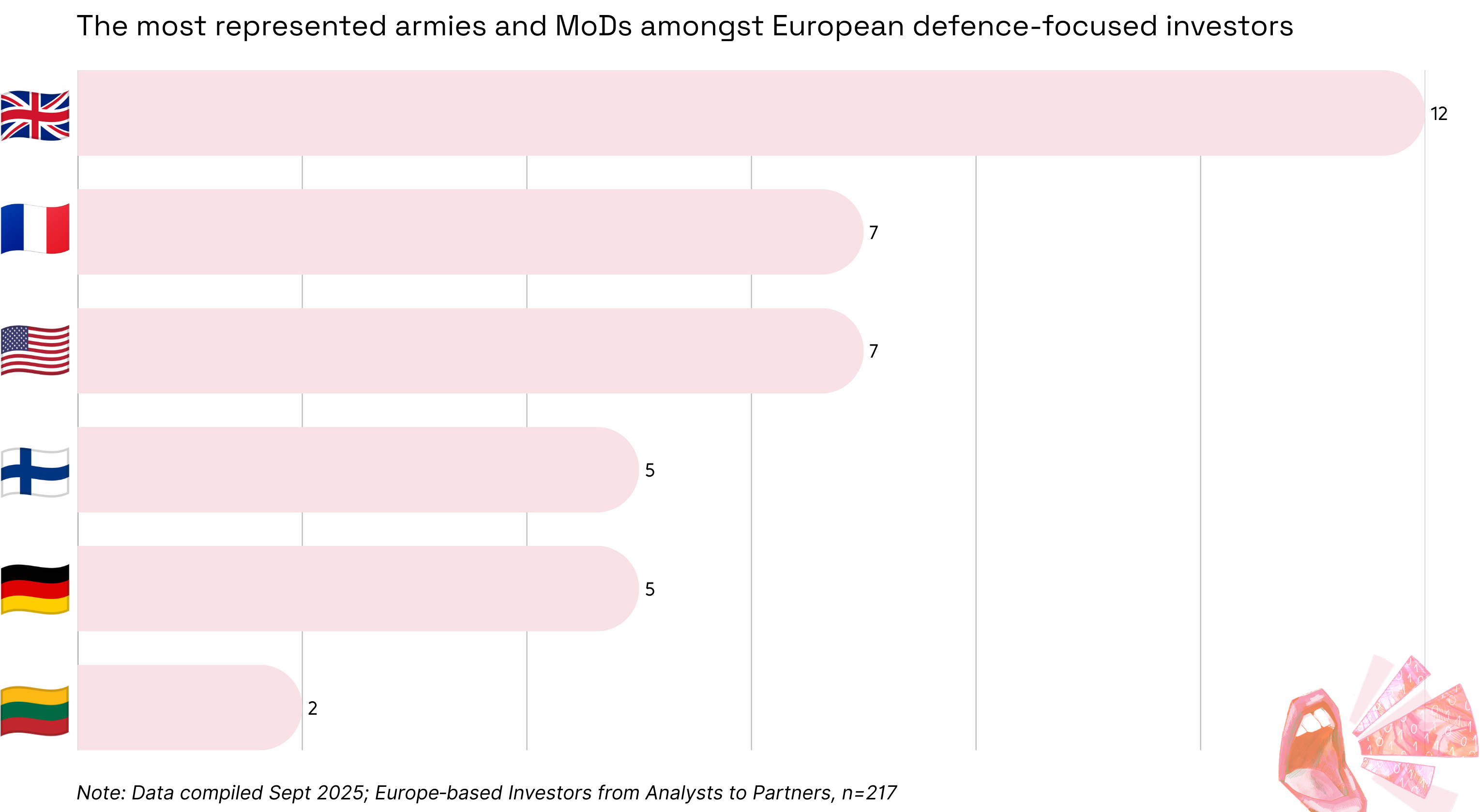

The people investing in the European defence tech sector

For our fourth and final mapping, we looked at the people pouring capital into the sector: the investors. We started by mapping 1.479 individuals working at one of the listed funds in roles from analyst and associate to manager, director, principal, and partner. From there, we narrowed it down to 217 who are defence-focused and actively investing in the sector.

Within that group, we identified 36 investors with an army or defence ministry background, which represents 16.6%. However, the split between fund types is striking: specialist defence funds lean heavily on military expertise, with 26% of their investors having relevant experience, compared to just 12% in generalist funds.

As proof, the most represented funds are NIF, MD-One, Tikehau Capital, Expeditions Fund, and Defence Invest2. Except for Tikehau, they are all fully focused on dual-use and defence tech, backing companies in cybersecurity, intelligence, autonomy, AI, quantum, and privacy.

Conclusion: A sharp rise in hiring needs across defence funds and scale-ups

We’ve now mapped the backbone of European defence tech: founders, C-levels, commercial leaders, and the investors behind them. We’re seeing hiring needs spike across funds and scale-ups, and more teams are actively looking for leaders with army or defence ministry experience.

That pathway has been standard in the US for years; our data shows it’s now taking hold in Europe in a measurable way. With fresh capital entering the market and more companies moving into scale-up mode, you should expect demand to accelerate, pulling even more mission-experienced talent into key seats across the ecosystem.

To track the shift, it’d be interesting to rerun this analysis in two to three years and see how far the share of talent with a relevant background has climbed.

And if you’ve got content in mind and want to back it up with data-driven insights, let’s talk. We’d love to collaborate.

Want to see how we can support your search? Visit our website to explore our services and learn what we can do for you.

These analyses are based on the list of companies and funds provided by Dealroom.

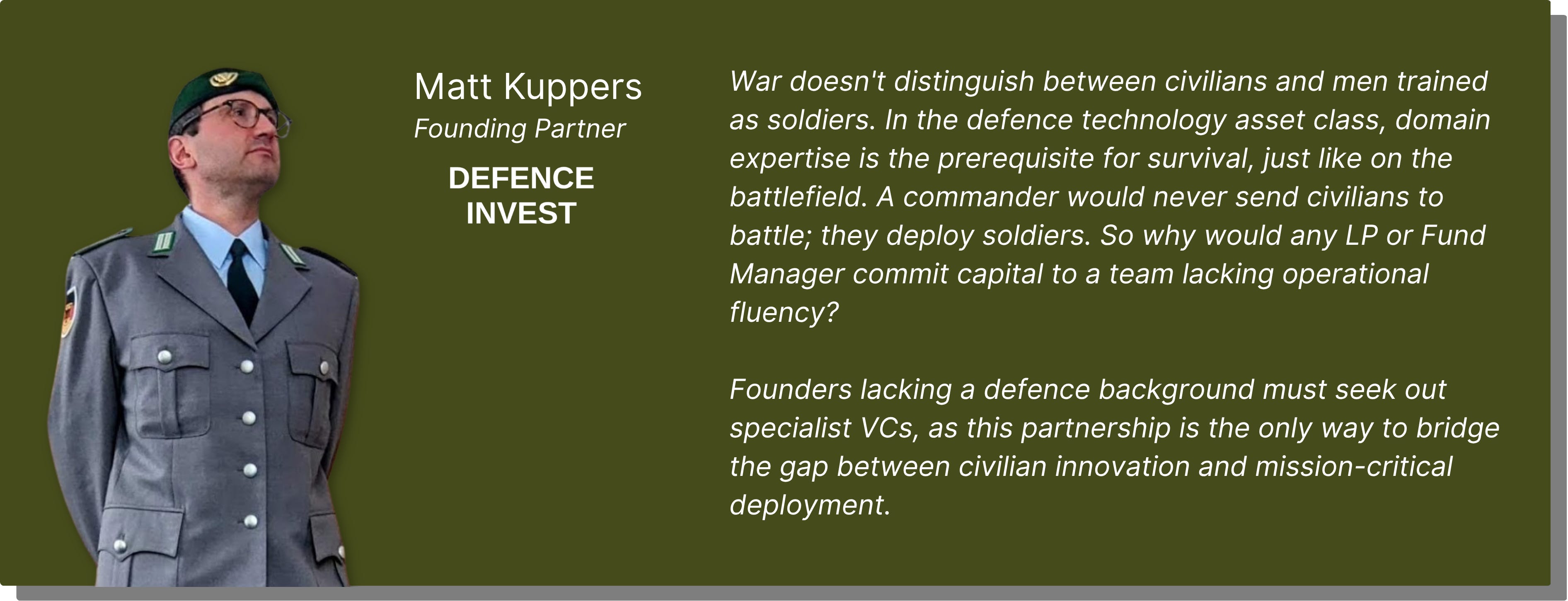

Defence Invest operates under a strict Defence-Only doctrine, backed by 60 years of combined military experience. Their conviction is that survival is based on skills, not wishes. This is why they exclusively invest in founders with verifiable defence backgrounds, to ensure capital is deployed against mission-readiness.