A Look at Europe’s Defence Technical Leaders by The Big Search x Defence Invest

We partnered with Defence Invest and mapped the European defence technical leadership talent pool.

Following the success of our previous defence talent analysis for Dealroom’s 2025 European Defence Tech Report, we continue our deep dive into the European defence tech ecosystem. This time, we’re focusing on the people actually building the products - the engineering, tech, product, R&D, and AI leaders.

Across our conversations with defence investors and operators, one theme kept coming up: the need for a triple-stack team. In practice, that means combining military knowledge (operations and procurement) with strong technical expertise. Most agreed that finding all three capabilities in a single person is rare, so they are usually spread across individuals.

If you’ve read our latest report (and we hope you did), you’ll remember that 14 to 16% of founders and investors have a military or MoD background. For a young sector, that is encouraging, but it also hints at how teams are composed: founders and investors often bring military expertise, while technical leaders have technical ownership. If that holds, the share of technical leaders with such experience is likely to be even smaller.

So, we set out to test it.

Using the same Dealroom pool of +600 companies, we identified 2,470 leaders from Head to C-level. That was a lot. Because the pool was heavily skewed toward prime defence companies, we narrowed the scope by excluding them and focusing on startups and scaleups. This left us with 697 leaders, 91.2% of whom are male.

We also partnered with Defence Invest1, who brought their military expertise and a fresh perspective. So, let’s get to the front line of the data and find out how many technical leaders actually have a military or MoD background.

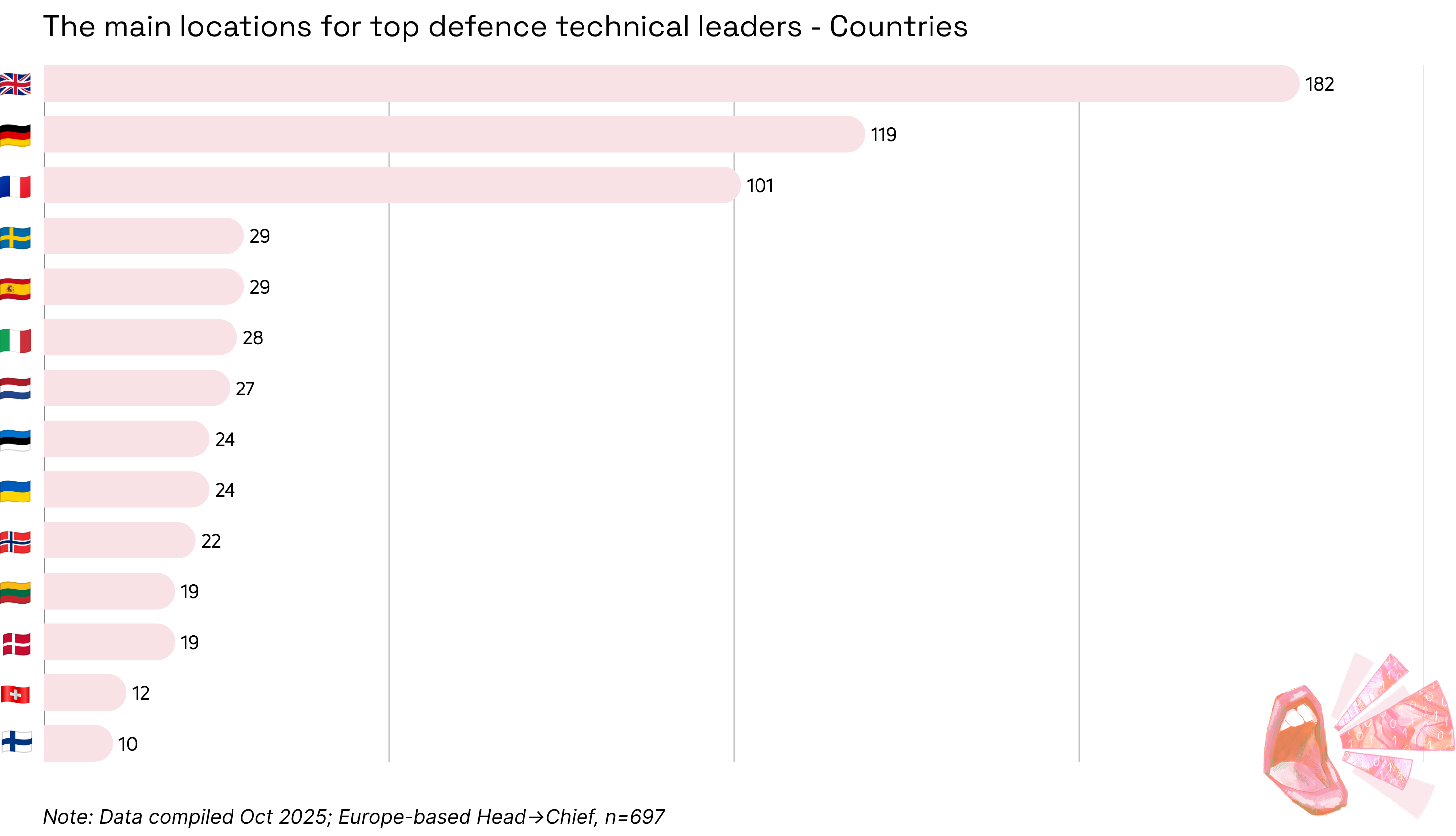

Where are Europe’s defence technical leaders located?

The United Kingdom, Germany, and France together account for 57.7% of the talent pool. That’s no surprise given that many of Europe’s most advanced defence tech startups and scaleups are based in these countries. According to Dealroom’s Defence Tech report, the top 5 European cities for VC investment in defence are in these Western European hubs, which naturally attract more senior technical talent.

Meanwhile, 16.2% of leaders are based in Eastern Europe. As one might expect, most are located in Ukraine and the Baltics. For the latter, the proximity to Russia and ongoing conflict put them under greater pressure to move faster. Latvia, however, remains absent, likely a reflection of its smaller startup ecosystem and less developed venture network, with local investors only recently beginning to prioritise defence as the regional threat environment intensifies.

In Ukraine, war has created founders, defence tech companies, and the technical leaders driving them. To get a closer look at the country’s ecosystem, we spoke with Denys Gurak, Co-founder and COO/CIO of MITS Capital2, who shared his insights on Ukraine’s growing defence tech landscape.

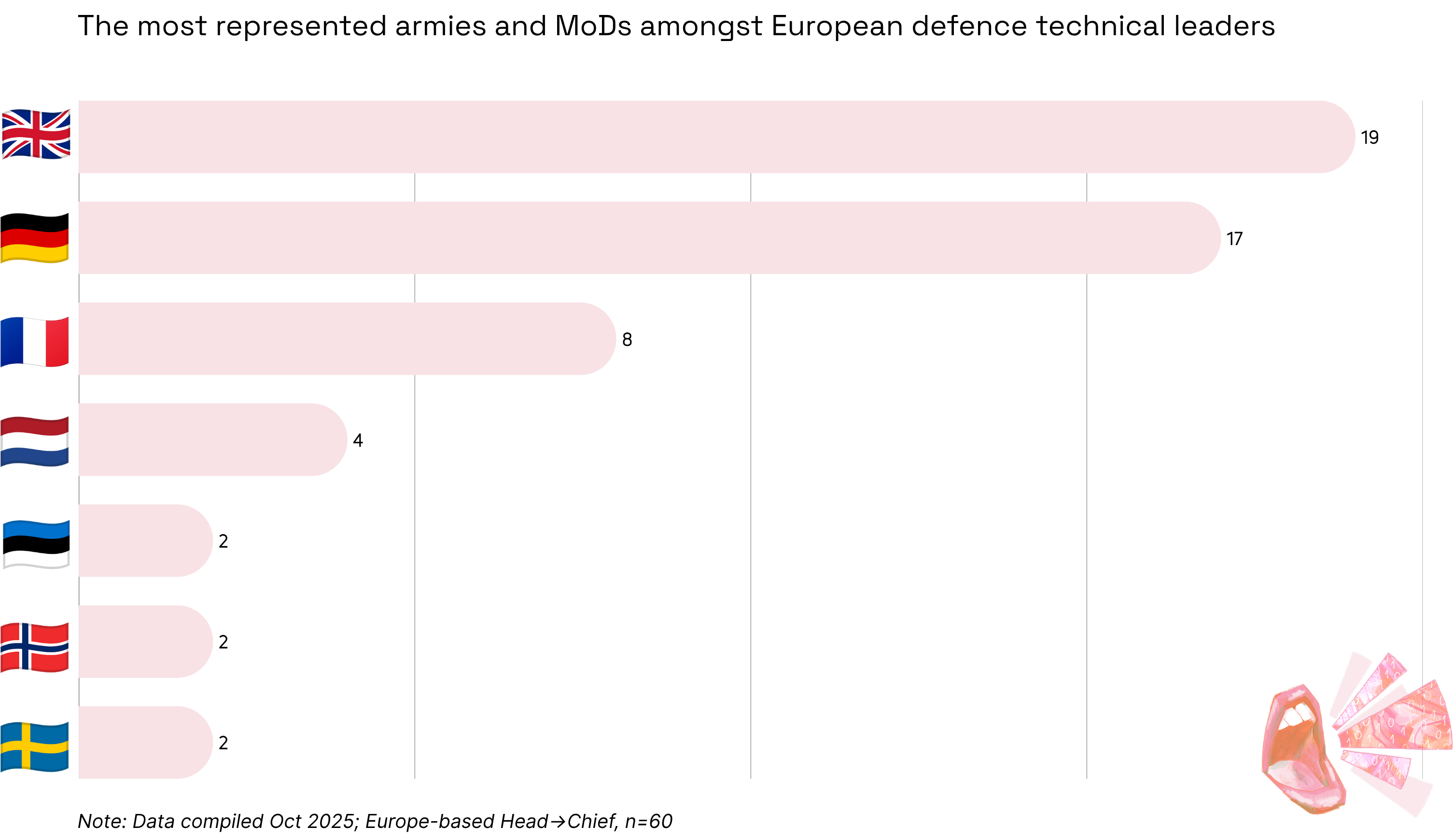

How many defence technical leaders have military or MoD backgrounds?

In total, we found 60 technical leaders with military or MoD experience, which represents 8.6% of the group. This supports our earlier point that success in defence tech today relies on building triple-stack teams. Founders and investors bring the military and procurement expertise, and technical leaders focus on product and engineering excellence. In that context, it becomes less essential for technical leaders themselves to have a military background.

The war in Ukraine has also made it clear that the nature of warfare is changing. Modern conflict is increasingly defined by electronic systems, drones, and intelligence capabilities, placing defence and dual-use technologies at the centre of national security. Yet great technology alone isn’t enough. To succeed, companies must also understand operational end-user needs and navigate the complexities of defence procurement and contracting - areas where experienced operators and ex-military leaders add significant value.

The current influx of capital into defence technology is rapidly exposing a critical flaw: the vast chasm between financial enthusiasm and operational expertise. Success in this sector is not defined by civilian software metrics; it is predicated on mission-readiness, a concept that demands intimate access to the defence establishment’s unique culture and processes. This environment often functions as an ‘old boys club,’ where trust, access to sensitive information, and operational credibility must be earned over decades of service, effectively shielding the core industry from financially driven, generalist approaches.

Vishal Gaglani from Defence Invest.

Thus, you can clearly see the value of people who know the system alongside strong technologists. This combination of skills is what turns innovation into capability and makes the difference between a breakthrough that reaches the battlefield and a startup that never leaves the lab.

Where do these technical leaders originate from?

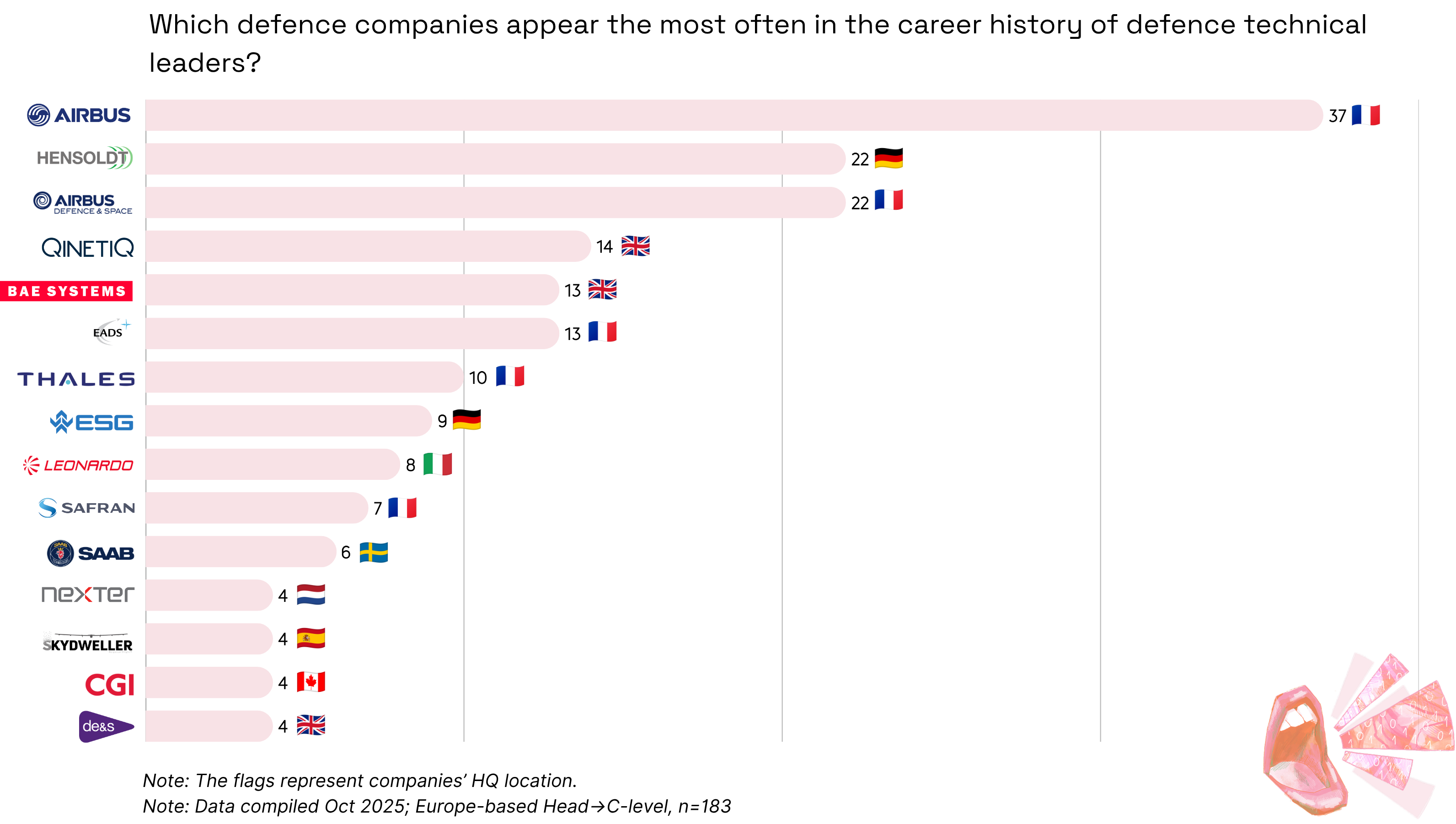

If there are only a few defence tech scaleups in Europe to hunt from and most technical leaders don’t have military or MoD experience, where do these R&D leaders come from?

To find out, we looked at their backgrounds and career histories for traces of prior defence experience. We found that 183 leaders, or 26.3%, had previously worked in defence companies. As you can see, the majority come from large industry corporates such as Airbus Defence, Hensoldt, and BAE Systems.

Europe still has relatively few defence-tech scaleups and an even smaller pool of people who’ve been on this journey from Series B to exit. As a result, defence-tech startups are increasingly drawing from the established defence primes, where talent already has deep technical expertise and, in many cases, active security clearances.

Matt Kuppers, from Defence Invest, explains that security clearances, which are a fundamental requirement for members of the armed forces and defence contractors, are non-negotiable for proper due diligence. Defence technology is, at its core, a matter of national security, and without the appropriate clearances, companies cannot access the classified information needed to fully vet a technology’s viability or conduct a true market assessment.

However, as more defence startups begin to scale, competition for this kind of talent will intensify. Unless a new wave of European scaleups reaches maturity and begins creating its own alumni “mafias”, startups will have to pay a premium to attract talent from the defence primes.

Yet, we’re already seeing early signs of this shift. Jan-Hendrik Boelens, former CTO at Quantum-Systems, left to found Alpine Eagle, a Munich-based company developing air-to-air counter-drone systems. A clear example of the next generation of leaders emerging from Europe’s growing defence-tech ecosystem.

Conclusion: the need for a triple-stack team

As the war intensifies, defence and dual-use technology companies are likely to play a key role in shaping the outcome. However, not all will succeed. The most successful and sovereign defence tech startups will be those that (1) build strong, differentiated technology, (2) understand operational realities and develop supply chains that meet defence standards while remaining cost-competitive, and (3) master regulatory and compliance challenges to deliver products effectively to the field.

Throughout this piece, we mapped the European defence technical leadership talent pool and found that these technical leaders may not bring military or MoD experience, but they carry valuable know-how from global defence players. In the end, within a triple-stack team, founders and investors bring military and operational knowledge, while technical leaders focus on product and engineering excellence - making it less essential for them to share the same background.

Much like many leaders from other DeepTech sectors, they’re transitioning from large industrial players to startups, channelling that experience toward strengthening Europe’s technological sovereignty.

For Matt Kuppers, defence expertise must serve a functional purpose: providing the unreplicable insight necessary to understand and navigate the opaque procurement processes of various Ministries of Defence, the strategic roadmaps of defence primes, and the intricate supply chain security standards. This foundational understanding minimises portfolio risk and ensures capital is channelled toward solutions that possess a genuine, expedited path to deployment, rather than being trapped in bureaucratic deadlock.

Want to see how we can support your search? Visit our website to explore our services and learn what we can do for you.

Defence Invest operates under a strict Defence-Only doctrine, backed by 60 years of combined military experience. Their conviction is that survival is based on skills, not wishes. This is why they exclusively invest in founders with verifiable defence backgrounds, to ensure capital is deployed against mission-readiness.

Founded in 2024, MITS Capital LLC is a Kyiv- and New York-based investment group focused on funding Ukrainian defence innovations. Its platform includes the MITS Accelerator, MITS Lightning Fund, an investment advisory unit, and MITS LAB Initiative, with a mission to bring global capital into Ukraine’s defence industrial base. According to the latest Ernst & Young report, MITS Lightning Fund is currently one of the largest international investors in Ukraine’s defence tech ecosystem. As of August 2025, MITS Capital has 11 portfolio companies, including Tencore, Teletactica, and NODRA Dynamics.