Europe’s B2C Fintech Unicorns: What Monzo and N26's Product Leadership Team Reveals About Their Growth

From London’s coral cards to Berlin’s banking license, what can we learn about their product talent leadership team?

Following the success of our analysis of Revolut's product organization last year, we turned our attention to the product leadership teams behind two other successful European fintech unicorns: Monzo, Britain's biggest digital bank, quietly preparing for an IPO, and N26, Germany's highest-valued fintech.

Product teams are central to the success of these digital banks, so we wanted to understand who drives product decisions for each company and how they approach building their product leadership teams.

A Quick History

Europe's fintech sector seems to be alive again. From Klarna’s postponed IPO to Revolut's continued blistering growth pace, as well as new entrants raising significant funding rounds (Upvest, Findmid, or Tebi OS), recent events have revitalized the market.

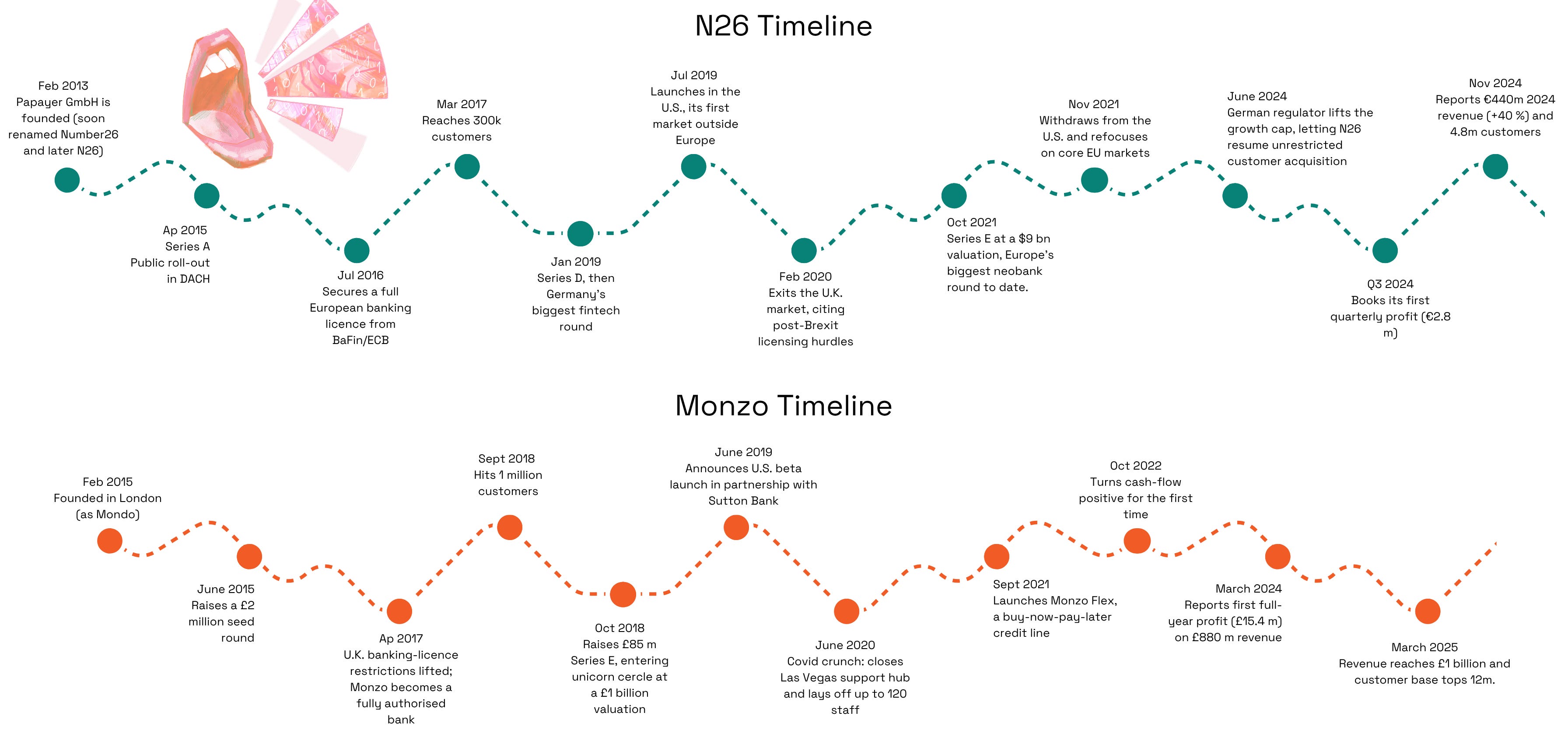

But it wasn't always so. Back in 2012, none of the most popular European digital banks today were even around. N26 was founded in 2013, Monzo in 2015, and Revolut in 2015.

Monzo has rapidly become Britain’s seventh-largest bank with over 12 million customers and €1b in revenue in 2024. N26 serves 4.8 million active users and generates €440m in revenue.

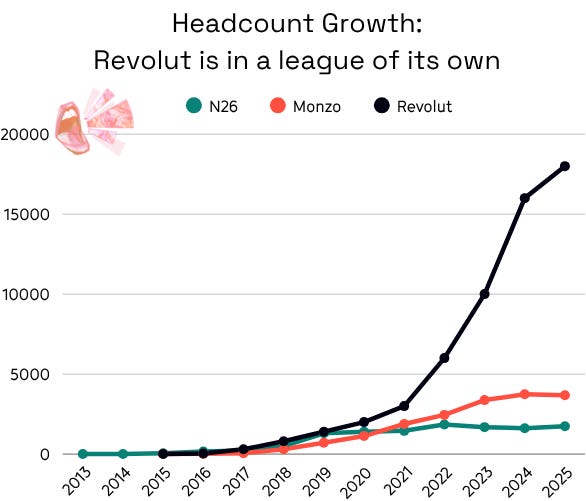

Today, Revolut is a juggernaut, counting 50m+ customers and revenues of €3.5b. It's in a league of its own.

Just look at how Revolut took off post-2020. The above chart shows headcount growth.

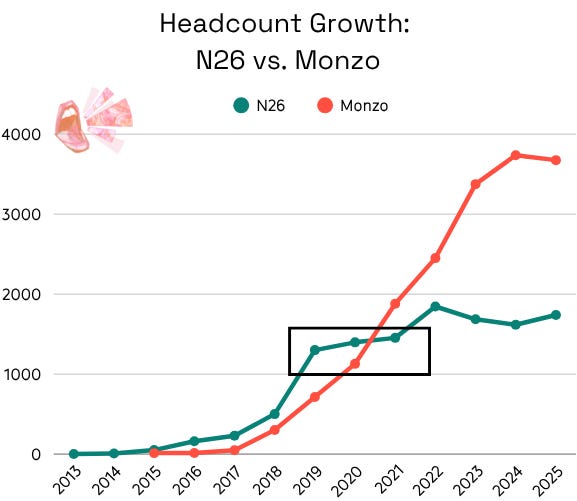

But this piece isn't about Revolut, so let's refocus on N26 and Monzo. Also, here, you can see that the two companies began diverging between 2019 and 2021.

Interestingly, N26 grew faster in headcount initially but slowed down significantly in later years. Between 2019 and 2025, it had a 5% annual growth rate. Meanwhile, Monzo had a 34% annual growth rate between 2019 and 2025.

So, what happened? We mapped some of the key milestones that both N26 and Monzo went through on their growth journeys.

Zooming in, we see two radically different approaches:

Monzo remained largely focused on its home market and improving the monetization of its existing customer base. It weathered the COVID storm by sticking to its core and doubling down. Currently, one in five British adults already use Monzo, but the company seems far from done and believes there’s still plenty of room to grow.

N26 tried to replicate Revolut's aggressive global expansion strategy, pushing hard on customer acquisition. But it ended up pulling out of the UK, citing Brexit. And then getting hit by BaFin fines and expansion caps in 2021 (limit of 60k new customer onboardings), ultimately also causing it to withdraw from the US. In 2023, N26 cut its global headcount by 4% and also scaled back its operations in Brazil. BaFin lifted the growth cap in June 2024, and since then, the company reported €440m of revenue in 2024 and a headcount growth of 5.5%.

How Did N26 and Monzo's CPO Role Evolve Over Time?

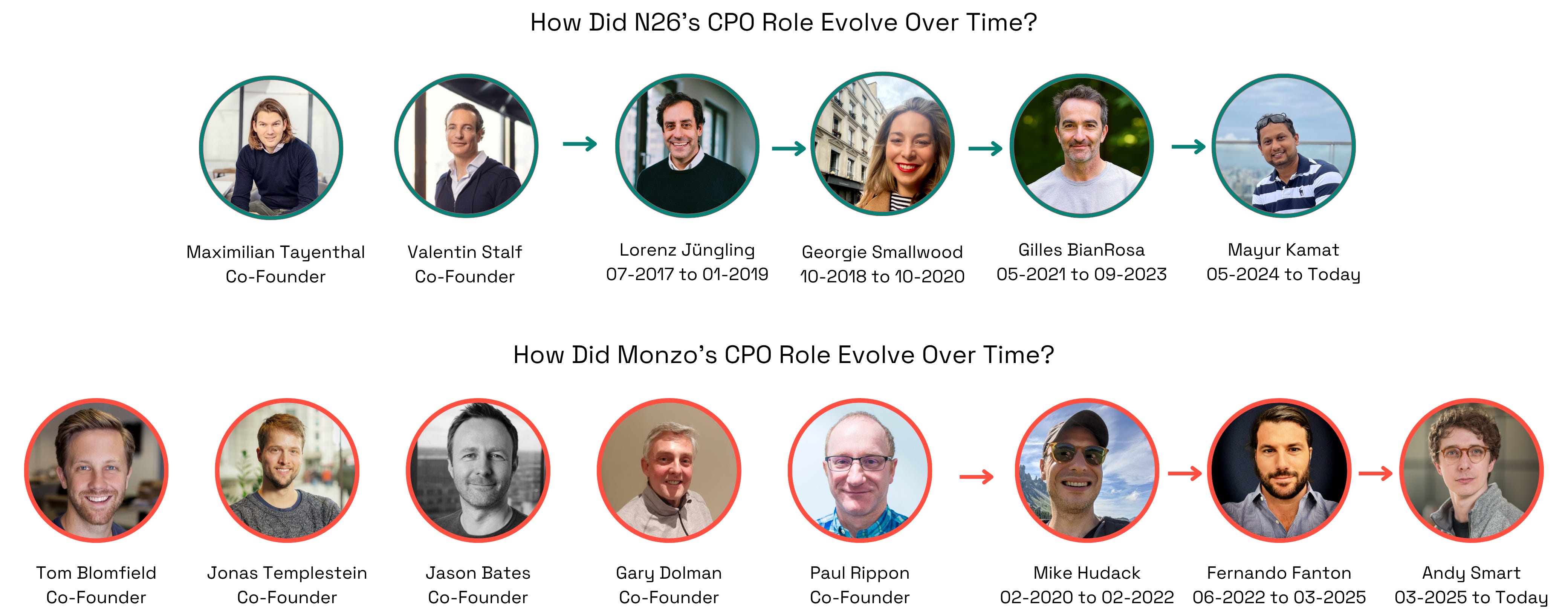

In the early stages, neither Monzo nor N26 had a dedicated CPO, with one or more co-founders likely handling product responsibilities. N26 appointed its first CPO four years after founding, while Monzo did so five years in. These early hires were among the first digital banking CPOs in Europe, as the sector didn't exist before:

Lorenz Jüngling (N26) had previously served as a partner at McKinsey & Company and N26's COO. He stepped into the role shortly after N26 secured a full European banking license. Key product milestones included the launch of insurance services within the app and 3D Secure support.

Mike Hudack (Monzo) had previously served as CPO/CTO at Deliveroo and Director of Product Management at Google. He joined during a more mature growth phase, when Monzo had already reached 1,000 FTEs. During his tenure, he oversaw the reintroduction of Monzo Plus and launched Monzo Premium and Monzo Flex, a BNPL product.

Other CPOs include:

Georgie Smallwood (N26) primarily had a B2C Marketplace background, having worked at REA Group, Australia’s biggest marketplace, and public company Scout24. She took over during N26’s UK market entry. During her tenure, N26 launched its Smart subscription, featuring extra cards, budgeting tools, and customer support.

Gilles BianRosa (N26), former CPO of SoundCloud and Samsung Electronics. He was appointed just before the company raised its Series E. Major product updates included the launch of N26 Crypto in Austria.

Mayur Kamat (N26) previously served as SVP and Global Head of Product at Binance, a B2C Fintech company in the blockchain and cryptocurrency ecosystem. He joined just before regulators lifted N26’s customer growth cap and the company posted its first monthly profit. On the product side, Instant Savings expanded to 13 more markets, and trading fees were eliminated entirely, allowing customers to buy stocks and ETFs for free.

Fernando Fanton (Monzo) primarily had a B2C Food background, having worked at Rappi and JUST EAT as CPO/CTO. During his tenure, he drove international feature expansion, including inbound SWIFT payments for personal and business accounts across 40+ currencies. Other product updates include the restructuring of Monzo’s subscription plans and the launch of Monzo Pension.

Andy Smart (Monzo) was promoted internally after joining Monzo in 2016 as one of Monzo’s first 20 employees (senior iOS engineer).

Did you see our leaderboards featuring the best training grounds for future CPOs and CPTOs?

Re-Tracing Product Leadership at N26 and Monzo

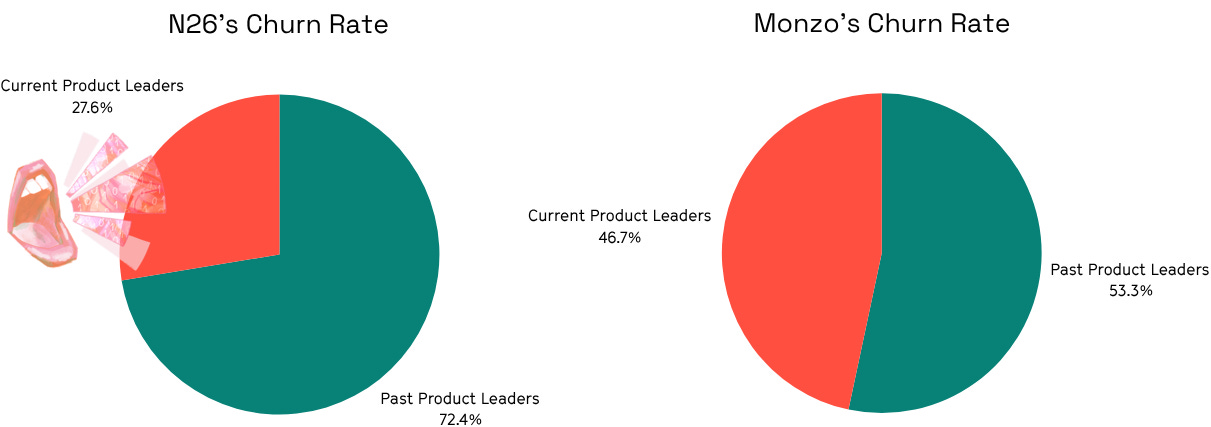

We focused on current and past product leaders at the C-, VP-, Director, and Head-level roles based in Europe and identified a total of 88 individuals (Monzo: 30, N26: 58).

Even though Monzo has nearly double the overall workforce of N26, we actually found fewer people in senior product leadership roles. And no, it's not just because Monzo is two years younger. For us, it likely indicates a higher turnover within N26's product team.

Product leader departures since founding: N26 at 72%, Monzo at 53%.

Average tenure within the company: N26: 2.3 years, Monzo: 3.1 years.

N26 has a noticeably higher churn rate (36% higher than Monzo's), and its product leaders typically stay ~10 months less. But let’s be honest, this isn’t breaking news. High turnover at N26 has been a talking point for years. From what we’ve found, it was likely driven by (1) the workplace culture, (2) structural problems, (3) lack of salary transparency, or under-market wages, and (4) lack of upward mobility.

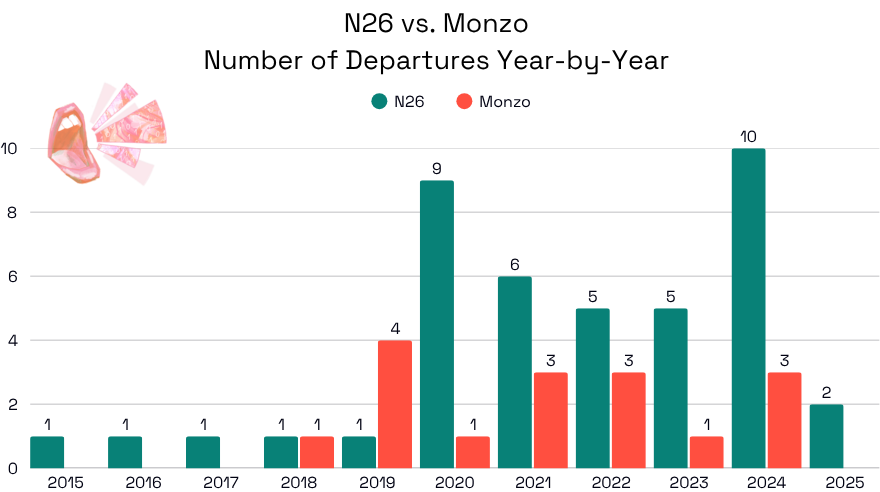

But when exactly did that turnover happen?

We took a closer look at when N26’s product leaders actually left the company, to see if there was any connection with the slowdown in its FTE growth journey, and we found something interesting. We identified not one but two clear waves of departures in the product leadership team at N26:

2020-21: This period lines up with the FTE slowdown we highlighted earlier. Former employees described a noticeable cultural shift as N26 entered its "hypergrowth" phase. An important wave of departures followed shortly after, especially within the product team. The primary reasons mentioned were a lack of clear product direction, a growing sense that autonomy was slipping away, and micromanagement from the C-suite.

2024: This period of high turnover seems closely tied to unmet expectations around a 2023 IPO. With those product leaders averaging about three years in tenure, many who joined during the IPO build-up likely decided to exit when those plans didn’t come through.

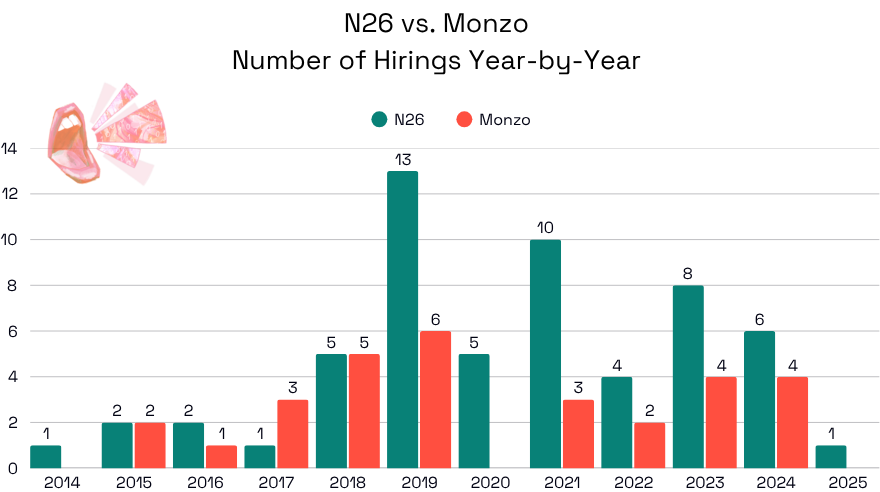

The Challenge of Hiring and Replacing 58 Product Leaders.

While Monzo's hiring seems to follow a planned approach to scaling, with ~70% of its recruitment happening within three months before or after securing new funding, N26's hiring has come in distinct waves:

The first major peak came in 2019, probably linked to the US launch build-out and the onset of its hypergrowth phase.

But the following surges, in 2021 and again in 2023–24, were reactive and followed the waves of departures mentioned previously.

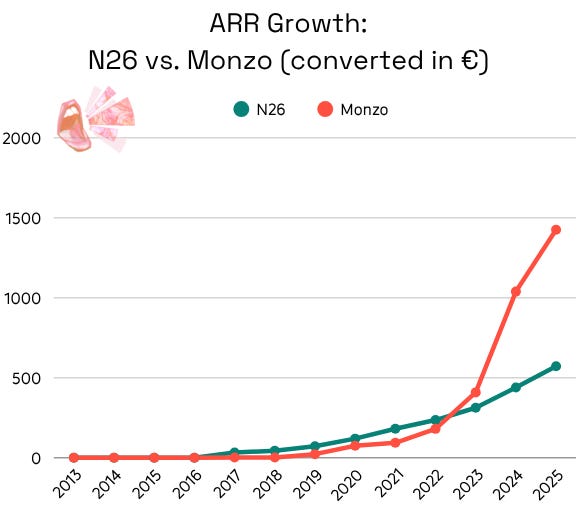

Beyond the obvious financial cost, high turnover takes a real toll on focus, continuity, re-onboarding, and institutional knowledge. It might also help explain the difference in ARR growth between the two companies.

Back in 2019, N26 reported an ARR of €72 million while Monzo sat at €23.5 million. In 2025, N26 is projected to hit €572 million with an ARR growth of 694%. Impressive, but Monzo is expected to reach €1.4 billion, representing an even more 5,900% growth.

When your team is stable, you can build your product steadily, ship faster, and scale more efficiently. But if you're constantly dealing with departures and onboarding replacements, that friction adds up, and it slows everything down.

Who Did They Bring In to Fill the Gap?

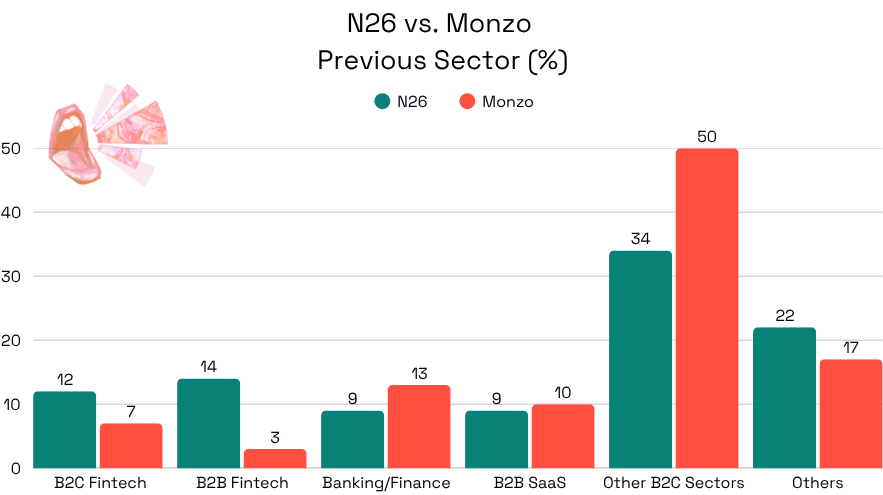

12% of N26 product leaders transitioned directly from other B2C fintech companies, whereas at Monzo, 7% did.

N26 seems to strategically prioritize pure-play fintech or banking/finance talent, even if they might have slightly less overall experience (13.4 years vs. 14 years at Monzo).

Over time, we’ve also seen N26 lean more and more into this focus. Before 2021 (excluding the year), just 24% of new product leaders joined directly from fintech or financial services. From 2021 onward (including the year), that figure jumps to 52%.

After the 2020-21 wave of departures, N26 seems to have recalibrated its hiring strategy and now targets fintech or finance/banking profiles. Probably an attempt to (1) support its "one account, many financial services, pan-EU" vision and (2) satisfy BaFin by bringing in more compliance-savvy leadership.

Regarding Monzo, the company hires like a consumer app and actively pulls in talent from B2C industries (mostly marketplace, food, and music sectors), which dovetails with its “turn banking into a daily consumer app” strategy. That background helps Monzo keep its banking interface closer to a shop-front app than a ledger and build an experience that feels familiar, engaging, and sticky. Additionally, Monzo leans heavily on British product leaders - 60% are UK nationals. This high proportion of British product leaders clearly lines up with its focus on growing its presence at home and grabbing more of the UK market.

Conclusion: Where Are They Today?

The products: Monzo, founded in 2015 as a basic current account product with a prepaid card, has since grown into a broader financial platform. It now offers diverse financial products like stocks and shares, BNPL, and is rolling out pensions. N26 has also expanded its product suite to become a universal bank. But it still lacks one major pillar of many competitors: business banking. It currently serves freelancers and the self-employed, but not enterprises.

Market Expansion: After an initial attempt to break into the US market, Monzo is giving it another shot, not by securing a banking license this time, but by partnering with Sutton Bank. It also brought in a new US CEO. Conversely, N26 is betting on a pan-European presence and currently operates in 24 countries, though 75% of its customers are concentrated in Germany, France, Italy, and Spain.

Who’s likely to IPO first and where? Back in 2021, profitability wasn’t a dealbreaker. That’s no longer the case. Today, turning a profit is a must-have for Fintechs looking to go public. On that front, both Monzo and N26 have checked the box. N26’s CEO has publicly suggested a timeline between 2027 and 2029. Monzo hasn’t officially said much, but its recent senior hires in finance at the end of 2024 suggest a more imminent move. With profitability achieved and market conditions looking more optimistic for 2025 (despite Trump’s nonsense), Monzo may well be eyeing the IPO window. Given its UK focus, London seems the most natural venue. For N26, it’s trickier. The company isn't active in the UK or the US, making London and New York less likely choices. Frankfurt is a possibility, but the IPO market there is limited; only four companies went public on the Frankfurt Stock Exchange in 2024.

Talent: Another major challenge for both will be acquisition and retention. In fintech, top talent can be prize hires. Right now, Glassdoor ratings offer some insight into employer brand: N26 scores 3.4 out of 5, with 57% of employees recommending the company. Monzo fares better with a 3.9 rating and 73% recommendation rate.

AI Adoption: Beyond support and personalization, Monzo is using AI to actively defend against fraud and enhance customer experience. Its real-time models now catch 95% of scams and have helped reduce fraud losses by 80%. N26 takes a different angle, positioning AI as the backbone of compliance. It leverages machine learning for AML monitoring, risk analysis, and service automation, framing it as the engine behind secure, scalable growth.

If this kind of mapping speaks to you, if you're curious how we built it, or if you're hiring a product leader, let's talk 🙂 Andrei Majewski

If you wish to access our exclusive data file with N26’s and Monzo’s product leaders, simply drop a message in the comments, and we’ll send it to you. 📥